The AI-Fed Catch 22: Tango of Technology and Policy

The market has been highly tuned to news from the Fed or developments in artificial intelligence technology to set expectations. Meanwhile, the robust U.S. economy continued to drive optimism in global markets despite stubborn modest inflation. Despite recent volatility, talk of recession has disappeared behind strong economic news and optimism over AI. But in the journey to reduce inflation, the last mile may be the hardest.

Markets

Market Performance

The first quarter of 2024 saw continued strong performance for equities, particularly in U.S. large cap stocks driven by resilient economic data and strong earnings. The MSCI ACWI and S&P 500 rose 8.2% and 10.4% respectively for the quarter. In contrast, bond markets were more affected by stickier-than-expected inflation, reducing expectations for rate cuts. By the end of the quarter, market expectations had shifted, with only three rate cuts priced in, down from six at the start of the year.

Amidst the ongoing dominance of U.S. large cap growth stocks driven by AI-related exuberance, the equity rally later broadened out, with U.S. small cap and value stocks both posting solid returns. International equities performed steadily, led by a 6.4% gain in the Asia-Pacific region driven by Japanese stocks. European equities returned 5.1%, while Emerging Markets returned 2%, underperforming because of the weak growth outlook in China.

Following strong gains in Q4, U.S. aggregate bonds were down 0.7% in Q1. Lessened expectations for rate cuts translated to the 10-year Treasury yield rising 25 bps to 4.2%, and over 3% losses in long-duration bonds. Treasury floating rate bonds outperformed due to their ultra-short duration, and high yield bonds thrived, benefiting from lower interest rate sensitivity and solid fundamentals. International Treasuries lost 3.7% due to a stronger dollar, but Emerging Market bonds gained 1.5% as high real yields prevailed.

Higher rates applied pressure on REITs, which fell over 1%, a major reversal from Q4. Alternately, gold shined in Q1, rising 7.7% as a risk hedge against economic uncertainty and geopolitical tensions.

The last quarter was a reminder that cash should be managed appropriately for the environment. The inverted yield curve suggested little return expectation for the interest rate risk, which proved harmful last quarter. On the other hand, Treasury Floating Rate Notes had higher yield with very little volatility, providing return without the need to bet against the Fed or markets. As cash remains a viable asset class, it is best allocated as part of an optimized portfolio.

Strategy Performance

All New Frontier's ETF portfolios delivered strong quarterly returns. Equity allocations contributed to the absolute return, while bond allocations contributed to the benchmark relative returns.

For Global Core, Treasury floating rate bonds and high yield credit bonds were the major contributors to the relative outperformance in Q1. However, the portfolio's underweight to the dominant U.S. large-cap stock rally, particularly in growth names, offset the benefits from bond allocations and global diversification. In the Tax-Sensitive portfolios, performance was in line with Global Core, with municipal bonds performing slightly better compared to their taxable counterparts, and high yield municipal bonds as the top contributor.

The Multi-Asset Income (MAI) portfolios experienced a positive quarter, although dividend stocks trailed behind the broader market. U.S. high dividend stocks and U.S. preferred stocks were the top contributors to the portfolio's strong relative performance. Currently, the MAI portfolios offer a yield of about 4.5% to 5%.

Model Reallocations

New Frontier rebalanced the Global Tax-Sensitive ETF portfolios and U.S. Core ETF portfolios on January 12. The Global Core ETF portfolios were rebalanced on March 7.

Reallocations: Models experienced significant asset class dispersion, for example large growth equities outperforming other asset classes, which contributed to the rebalancing decision. Furthermore, risk and return estimates changed due to market dynamics and particularly in response to significant changes in interest rates for government, municipal, corporate, and high yield bonds. Across models, allocation to U.S. equities increased slightly (approximately 2%) to align with the global market environment.

Global models additionally reduced exposure to credit risk, particularly through high yield ETFs, while keeping duration exposure consistent. Switzerland was removed from the portfolios after being introduced in 2011 to manage eurozone currency and debt risk.

Tax-sensitive models optimized differences between municipal and Treasury yield curves. Overall, tax-sensitive portfolios shifted to Treasurys from municipal bonds particularly Treasury floating rate notes compared to short-term municipal bonds due to their higher after-tax yields.

Tax consequences: Consistent with New Frontier’s policy, the tax-optimized rebalance is expected to result in no short-term gains and only modest long-term capital gains for most investors, as equity allocations were adjusted to manage embedded capital gains while maintaining optimal equity risk exposures.

New Frontier uses the Michaud-Esch portfolio rebalance test to guide portfolio reallocation and rebalancing decisions. This framework allows us to simultaneously consider changes to the risk characteristics of portfolios from price movements, and changes to optimal portfolio exposures from new capital market expectations.

Insights

Investment Themes

Though next quarter’s market will likely differ, little has fundamentally changed in the investment landscape from last quarter. The economy remains healthy, but with high interest rates and inflation above target. U.S. valuations remain high with optimism about the future and little concern for recession while the economic outlook for much of the rest of the world slowly improves. But while the landscape has changed little, sentiment has changed significantly—dramatically lower expectations for rate cuts.

Yet markets remain optimistic with little discount for the possibility of an economic slowdown. Therefore, equity risk may be higher than visible today. Fixed income, on the other hand, has known risks with interest rates in flux, the Fed evaluating rate changes and global inflation uncertainty. A less inverted yield curve is still inverted and begs the question of what the ultimate equilibrium will be for interest rates.

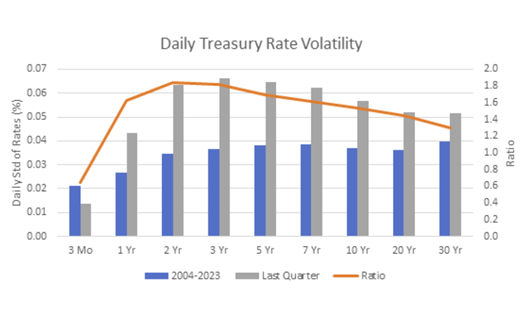

Despite (or perhaps because of) no changes in the policy rate, interest rate volatility remains elevated compared to long term levels.

Source: New Frontier, treasury rate data from treasury.gov

Fed watch

Markets are still focused on anticipating Fed policy and therefore, inflation still matters for moving markets. Markets fell sharply when inflation readings came in 0.1% higher than expectations. Whether or not this is an overreaction, these small differences, combined with strong employment data, may be enough to prevent the Fed from lowering rates and providing some relief for debt-dependent parts of the economy.

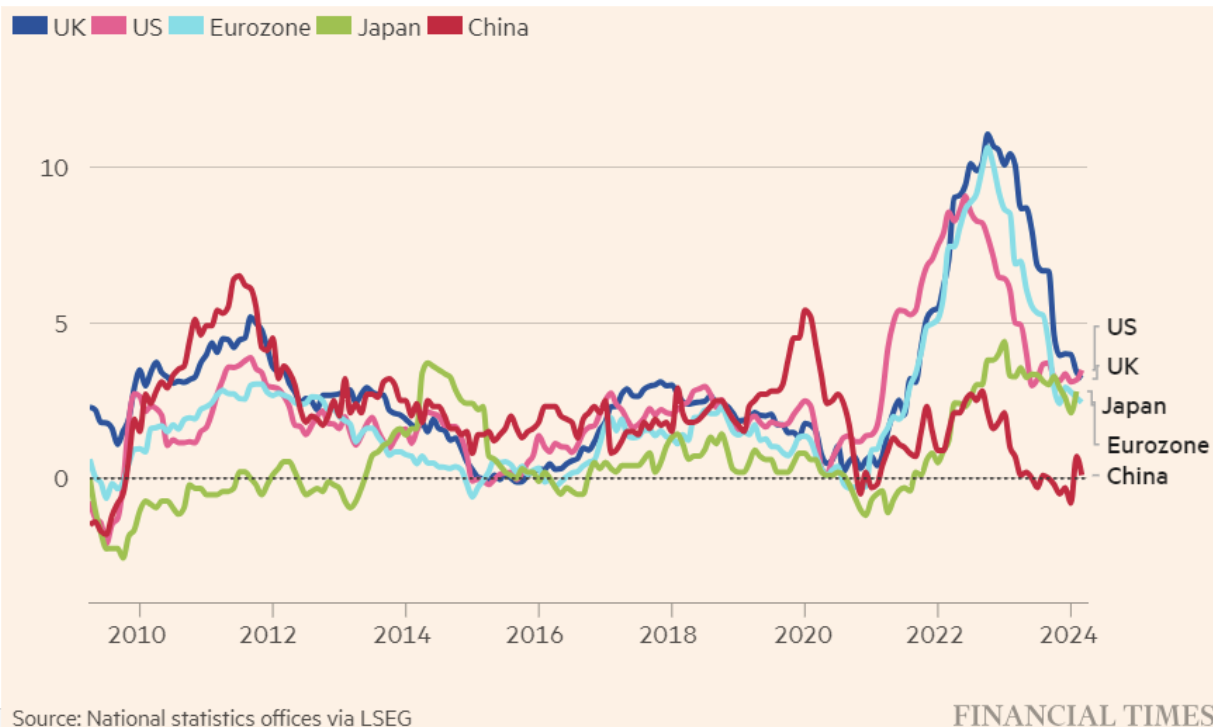

There is concern that inflation has slowed moving in the right direction globally, with the U.S. and the eurozone making little progress.

CPI as of 03/2024, except Japan as of 02/24.

The market’s inflation paradox

Markets cheer lackluster economic news in anticipation of rate cuts to spur future economic growth. But intuitively, it should be at least as good for economic growth in the present. It is not clear how an economic slowdown followed by lower interest rates would be more beneficial to the market value of equities than sustained economic growth.

Expectations for a successful soft landing remain dominant, but the possibility of “no landing” has come into focus. In this case, inflation may persist, short term rates may not fall, and the economy could continue to prosper. Whether this would be good for markets is unclear—eventually, inflation, a tight labor market, and high borrowing costs are likely to have an impact on corporate profits.

The Fed and Rates

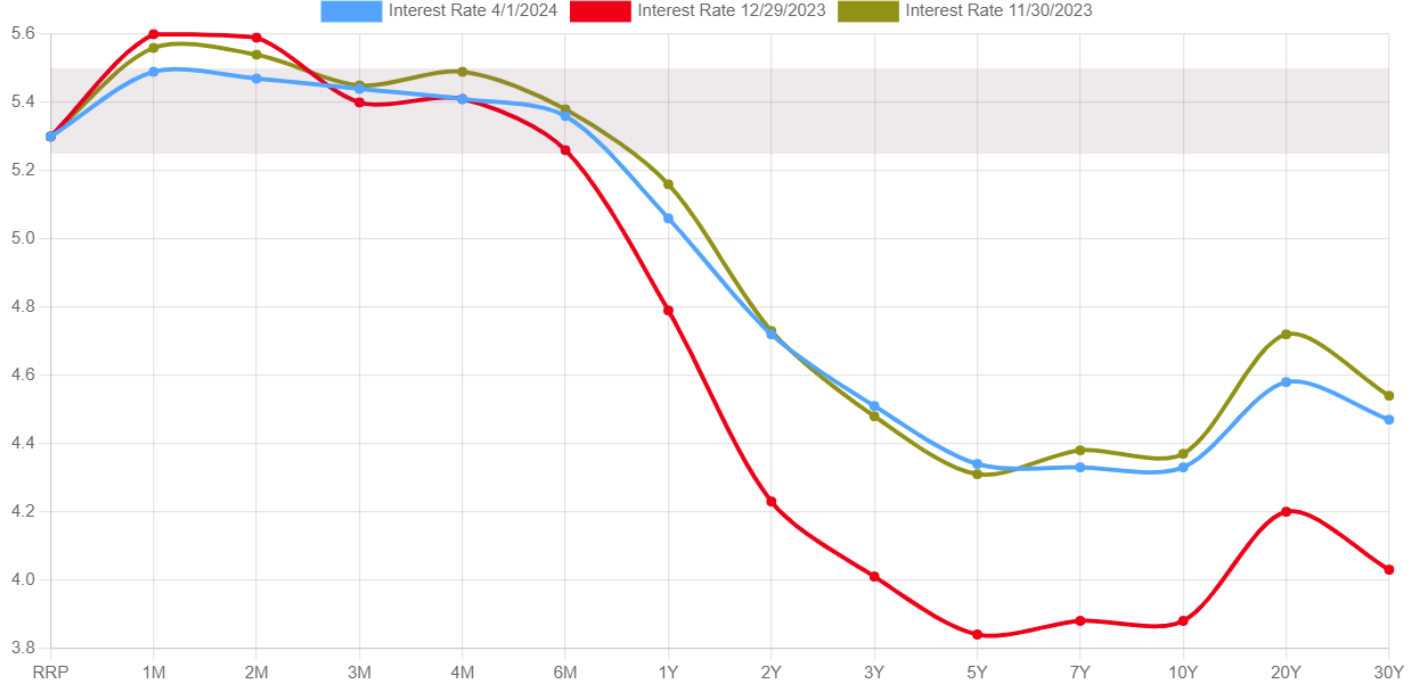

Source: U.S. Department of The Treasury

Comparing the yield curve this quarter (blue) to the beginning of the year quarter (red), we see little change in the short end of the yield curve, but significant increases in longer-term rates. This matches what we have seen in interest rate volatility, which has been low for short-term bonds as there have been no changes to interest rate policy, but high for longer terms as expectations about future rate policy changes. Note that interest rates have returned to levels similar to last November (green), before markets became optimistic about falling inflation.

AI Continues Driving Markets

Investors tend to focus on a small number of themes at a time and move markets according to how they fare. Other than inflation and the Fed, markets are focused on the development of AI and who will benefit from it.

Bubble or not?

Ultimately, the massive capital shift to AI will affect investors. One possibility follows the internet bubble, where investors indiscriminately provided capital to ideas, good and bad, so long as they were tangentially related to internet technology. Should too many questionable firms take advantage of investors’ enthusiasm for AI, investors may lose even if AI ultimately proves to be economically viable, as the high cost of inefficiently allocated capital could take decades to provide a reasonable return. On the other hand, massive investment in revolutionary ideas need not prove excessive. Railroads, for example, provided extraordinary returns which eventually normalized without a financial bubble.

Longer term, AI will likely have broad impact into other industries such as biotech and film as it broadly enhances productivity, potentially replaces white collar workers, and occasionally revolutionizes an industry. Therefore, there’s reason to expect that other asset classes will benefit as the technology bolsters smaller firms and those away from Silicon Valley.

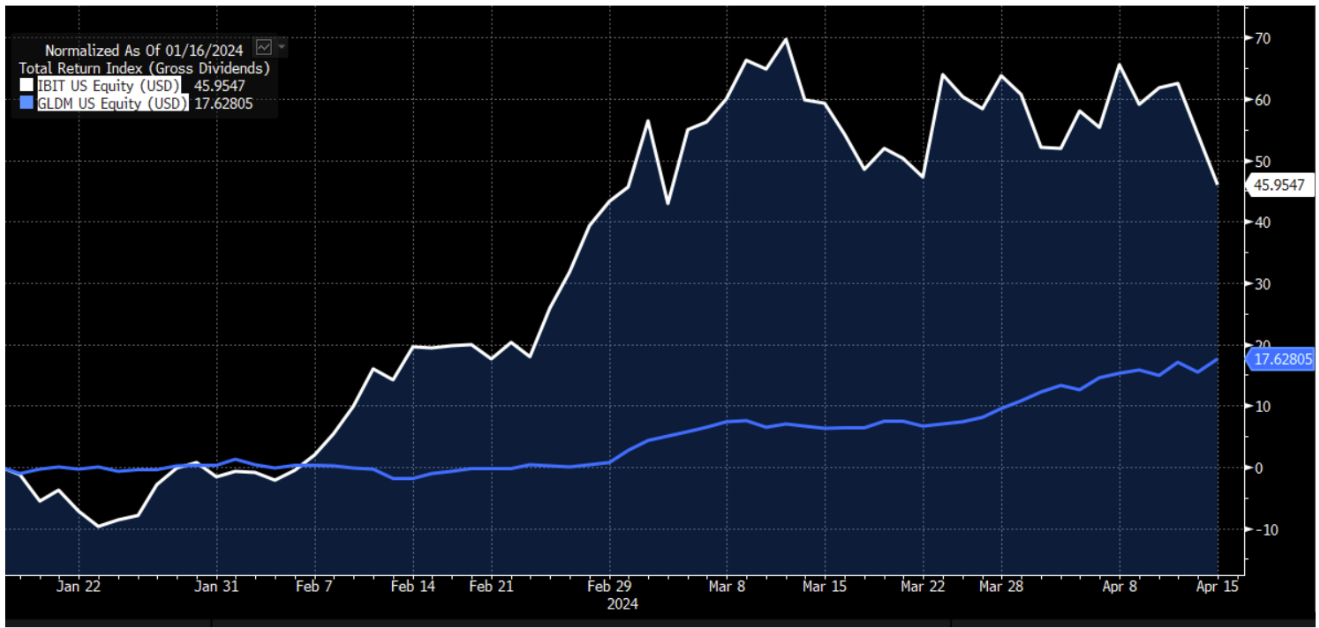

Gold and Bitcoin fared well last quarter, a period of geopolitical turmoil along with debt and inflation concerns, although bitcoin was a far less reliable risk hedge. It has long been our view that gold’s unique diversifying properties make it a useful component of a portfolio (Michaud, Michaud and Pulvermacher 2006). Bitcoin, however, failed as a risk hedge when it fell precipitously in response to recent Iran-Israel conflict. Bitcoin’s basic risk character is still unknown, and it is not yet clear whether it is defensive, procyclical, or even ultimately a store of value.

Source: Bloomberg

Private debt and equity are fashionable right now, but investing in these asset classes is more about picking the right fund and hoping for good results than improving portfolio efficiency. Recent popularity was catalyzed by the performance of private debt in 2022 as well as the launch of numerous private debt funds. The case for private investments typically relies on return expectations greatly in excess of standard public investments. But the performance of individual private equity funds is notoriously unreliable, and high dispersion in returns increases the likelihood of investors failing to meet their goals. While the fees of private investments have remained reliably high, their performance has not.

Other Insights

- Isolationist politics: while it is too soon to speculate on the presidential election, a shift towards greater isolation for the U.S. could make international diversification more valuable since the reduced economic correlation could lead to financial markets decoupling as well.

- A Government shutdown was again averted at the last minute. This is most notable for the lack of attention it received, but the problem will only become worse in the future as debt continues to rise.

- Debt to GDP will likely continue to rise as positive real interest rates mean the real debt of the country is accelerating.

- China has been trying to get out of the investor confidence crisis that has been driven by falling population, a deepening property crisis, ongoing deflation, high debt, and the government’s reluctance to intervene through stimulus or lower rates. Economic growth has been moderate, but government policy remains unsupportive of investors. But is it cheap enough to invest in?

- Japan is booming despite the weakening Yen. Even dollar terms, the Japanese market is one of the best this year, thanks to positive economic developments.

- Bitcoin ETFs work as intended, closely tracking the spot price and making Bitcoin an accessible asset class. Net inflows exceeded $10B but it remains highly volatile.

- CDs and savings accounts rates are good compared to recent memory, but generally less than comparable yields from risk-free (and state tax exempt) Treasurys. Optimizing allocations to cash along with the rest of the assets in a portfolio is conceptually more efficient than separately holding cash.

Conclusions

While the risk of economic slowdown should never be ignored, the U.S. continues to have the highest expected growth rate of any developed nation. It is therefore no coincidence that the U.S. also has among the highest interest rates, strongest currencies, and highest valuations for its corporations. The market knows this, of course.

Fiscal policy is known to take time to impact the economy, but more than two years after the first rate increase in March 2022, we are still looking for an identifiable effect. This begs the question whether the interest rate hikes are likely to be effective at reducing inflation. If inflation is clearly moving in the wrong direction, the Fed could raise rates further—after all, few economists doubt the efficacy of sufficiently restrictive policy. However, the more likely scenario remains in the ambiguous zone, where the risks of too much confound the risks of too little intervention.

Measuring success

Should you follow a benchmark when the benchmark is concentrated? The market portfolio is an average of all investors’ portfolios, but not necessarily the right portfolio for anyone. To provide value to their investors, asset managers need to deviate from the market portfolio, so some tracking error to a benchmark is inevitable. How much tracking error is desirable relates to the composition of the benchmark. If markets are highly concentrated in a handful of stocks, as they are now, higher than normal tracking error should be expected for a risk managed portfolio. Concentration can create great wealth quickly, but diversification is the key to long term wealth appreciation.

Asset managers should always attempt to achieve the highest return possible for their investors, but they need to prioritize what they know about risk over what they think they know about return. This is sound practice, followed by the largest and most sophisticated investors, because it is the key to long-term wealth appreciation. Investors should not be disappointed with recent positive returns for their portfolios if they were invested in an appropriately risk-managed portfolio.

DISCLOSURES: Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including loss of principal.