Q4 2023 Market Perspectives: The Turning Tide

After two years of fighting inflation amid fears of recession, markets and policy makers appear unified in their sanguine outlook. While interest rate increases designed to slow economies may well be nearing an end, markets are never without risk. The final quarter of 2023 marked a change in expectations, and economic inflection points are a time to think deeply about what’s driving markets.

Insights

Investment Themes

Market sentiment and security prices are currently dominated by expectations of a “soft landing” – a return to target inflation without the normally accompanying economic hardship. This has implications: short term rates will begin to fall; riskier assets should benefit from the greater certainty; and ultimately, the yield curve should “normalize” with higher rates for longer maturities. Additionally, both nominal and real yields are significant and positive. These set the strong expectation for positive returns for both stocks and bonds going forward.

However, there is always risk in investment, and a specific market scenario is never certain. In particular, a recession is still possible. An optimistic market may both underestimate risk and overestimate expected returns for equities. The actual risk may be higher due to the underrepresented likelihood of a recession, while future equity return expectations may be lower because of the high valuations of equities perceived as relatively safe.

Selling momentarily unfavorable asset classes can backfire. Over the fourth quarter, many of the year’s earlier investment trends reversed with high returns for small cap stocks, long duration bonds, and REITs.

Stocks, Bonds, and Cash

Despite the optimism, stocks remain the main driver of long-term return. Bonds, however, are measured on their ability to provide return and dampen risk. With higher yields, the potential future return from bonds is higher. Importantly, real rates are positive and historically high (1.7%/1.9% for 10/30-year as of 12/31). Additionally, bonds may benefit the portfolio as a hedge against a recession.

Cash should be managed appropriately for the environment. The inverted yield curve continues to suggest little return premium for interest rate risk. With cash remaining among the higher-yielding asset classes with very little volatility, Treasury Floating Rate Notes, for now, remain a useful source of return without the need to bet against the Fed or markets. Generally, asset classes worth investing in are best allocated as part of an optimized portfolio.

The Problem with Market Concentration

Asset managers should always attempt to achieve the highest return possible for their investors, but they need to prioritize what they know about risk over what they think they know about return. This is sound practice, followed by the largest and most sophisticated investors, because it is the key to long-term wealth appreciation. Investors should not be disappointed with the positive returns of 2023 for their portfolios if they were invested in an appropriately risk-managed portfolio.

What finance can do effectively is manage risk. While there will always be a concentrated portfolio that outperforms a diversified one, much has been made of the spectacular return of seven technology giants positioned to benefit from artificial intelligence. This is reminiscent of the concentration of technology companies positioned to benefit from the internet in 2000. While each of today’s tech giants clearly has tremendous economic value, they also clearly risk not meeting their extraordinary expectations. The fact that many of the biggest companies of 2000 suffered serious losses in the dot-com crash, and the Magnificent 7 fell 39% just the year before, highlights the uncertainty of their future returns.

The concept of market equilibrium dictates that efficient markets rapidly incorporate all available information until buyers and sellers agree on a price to which they are indifferent. This makes it difficult to generate higher returns through the selection of an asset or even broad asset class. The default assumption should be that return expectations for last year’s winners should be average going forward.

Risk, however, is persistent and therefore somewhat predictable. Rather than hoping for asset managers to consistently pick winners, relying on them to manage risk is more likely to lead to success. We do not invest with hindsight, and betting on the performance of a concentrated risky set of stocks is not prudent today or even a year ago.

Asset managers should always attempt to achieve the highest return possible for their investors, but they need to prioritize what they know about risk over what they think they know about return. This is sound practice, followed by the largest and most sophisticated investors, because it is the key to long-term wealth appreciation. Investors should not be disappointed with the positive returns of 2023 for their portfolios if they were invested in an appropriately risk-managed portfolio.

Long- vs. Short-Term Volatility

We see continued dramatic movement at all horizons on the yield curve. The persistent volatility in fixed income, particularly long-term fixed income, can seem perplexing. After all, interest rates over the next few months should matter very little to the holder of a 30-year bond. Long-term rates are better understood as expectations about a highly uncertain distant future. In this context, small changes in expectations today could have dramatic implications for the future. Here long-dated bonds are similar to equities—their true but unknown value is scarcely affected by economic conditions in the near future, but perceptions about what the future may look like can change easily.

The way risk affects valuation of long bonds and long-lived stocks explains why they tend to be negatively correlated when certain risks are present. For example, if the long-term economic reality worsens, this should hurt equity holders and relatively benefit bond holders (so long as the growth is not accompanied by an increase in inflation). Similarly, if the future economy exceeds expectations, stockholders should clearly benefit, whereas bond holders will likely lose as rates rise with increased demand for capital. Therefore, long bonds can improve efficiency of an optimized portfolio if their yield is sufficient.

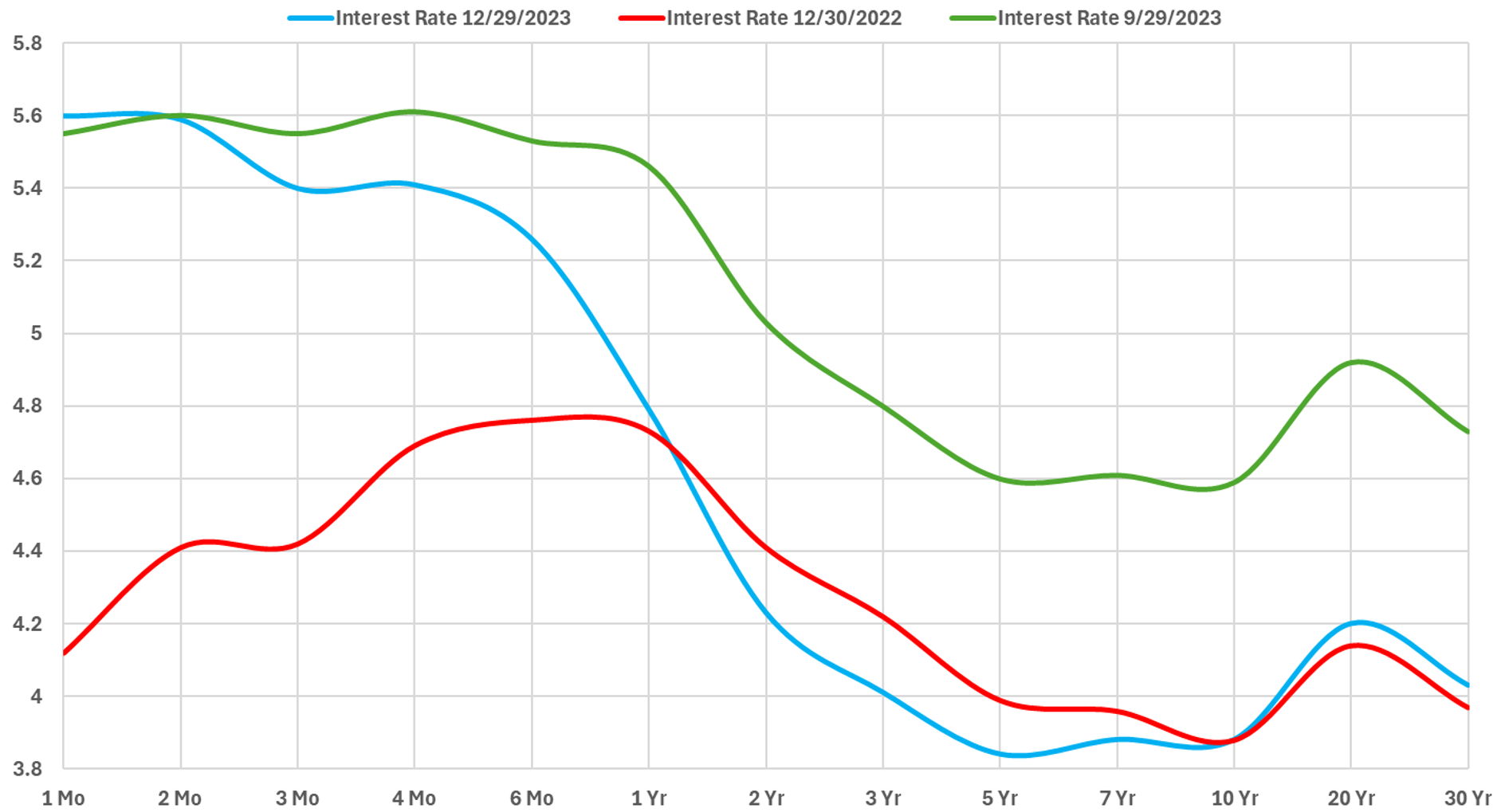

The Fed and Rates

Source: U.S. Department of The Treasury

Comparing the end of quarter yield curve this quarter (blue) to the third quarter (green), we see little change in the short end of the yield curve, but dramatic declines in longer-term rates. This is in contrast to the changes between now (blue) and a year ago (red) where short rates rose dramatically, but longer rates were nearly unchanged. If investors had not paid attention to markets over the year, they may have perceived an orderly response to the Fed raising short-term interest rates. However, rates were highly volatile in 2023.

The Fed controls the short-term risk-free rate, but markets determine longer rates. As always, market prices are a complex equilibrium from many participants. Market prices do not represent a belief in a single scenario, but rather an average of many expectations and preferences. For example, low yields in the future may be due to investors expecting to profit from those positions or others looking to hedge risks in the future.

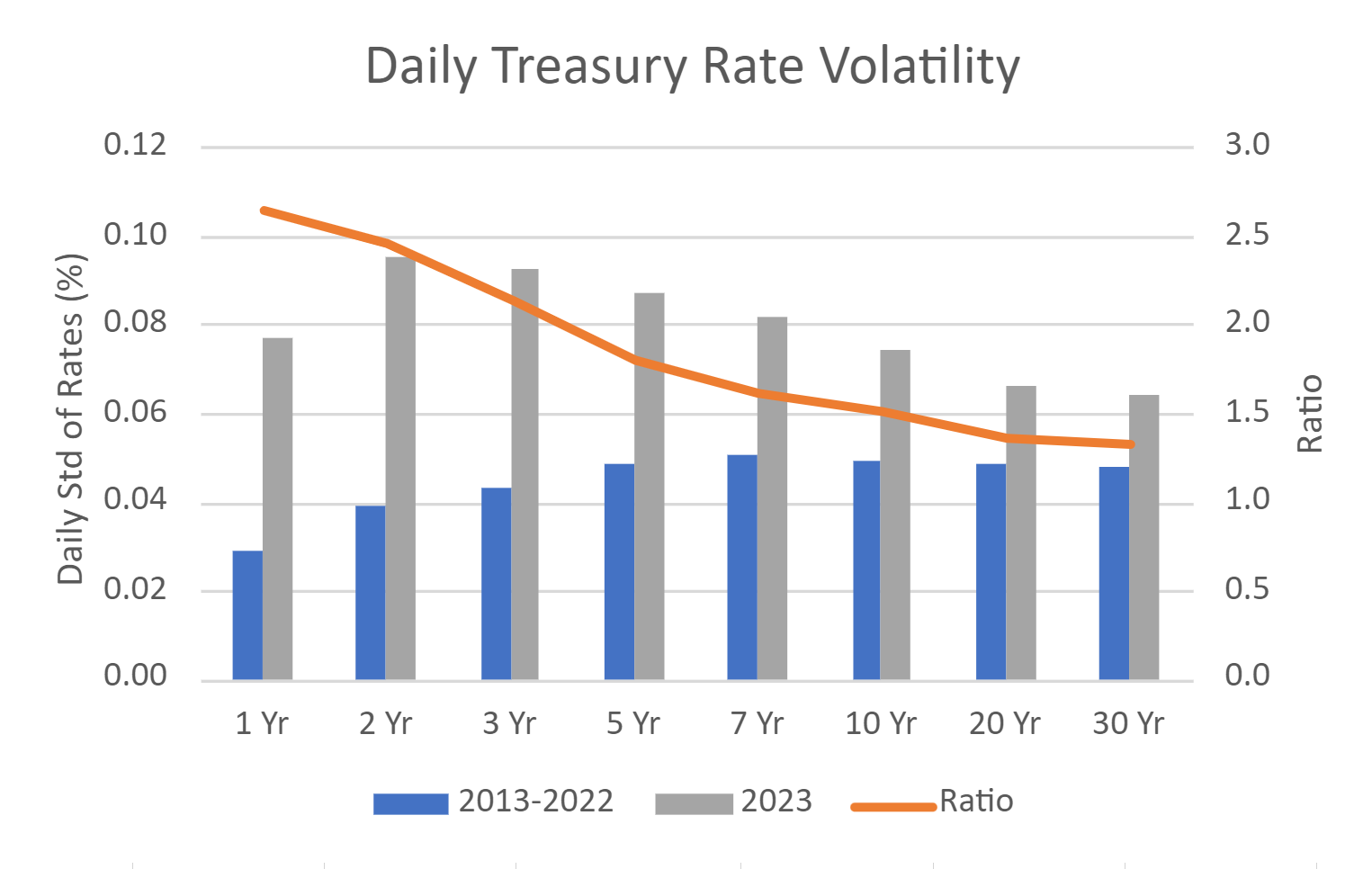

Fixed income volatility

Though lower than 2022 (not shown), 2023 fixed income volatility is still elevated relative to historical norms.

Source: U.S. Department of The Treasury

Debt and markets

With rising interest rates and the spotlights of politics, debt has come back into focus. It should be noted that much of the rhetoric and predictions of doom of the last 15 years was based on a flawed understanding of economics and did not come to pass. However, just because the impact of debt isn’t obvious doesn’t mean it’s irrelevant. We noted an increase in fixed income volatility compared to historical norms. A concern is that the higher debt levels may systemically increase risk for fixed income, which may require investors to adapt to the changing reality.

Geopolitics

2024 is a year of elections. This is particularly notable in the U.S., but globally, more than half the world’s population will choose their own leadership. History has shown little statistical difference in economic or market performance based on the political party in control. The implications may have long-term social and even economic implications, but markets tend to be surprisingly rational with respect to dramatic and emotional events. Notable examples of muted market responses to major geopolitical events include the past two presidential elections and the Russian invasion of Ukraine. The prudent approach is to analyze carefully, but not to overreact.

The Economy

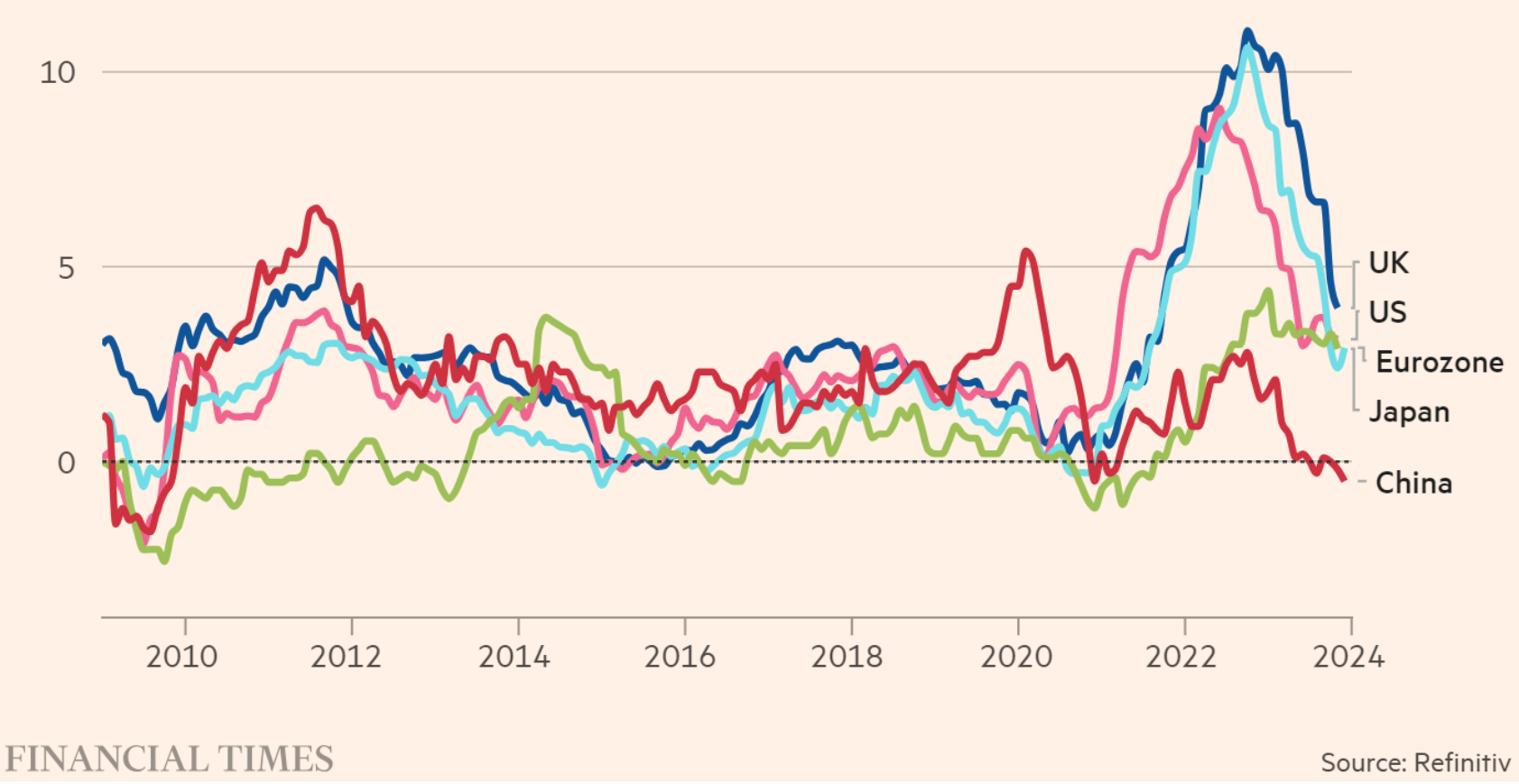

Inflation continues to move in the right direction globally, apart from China which faces deflation, at the annual rate of 3.4% (CPI) in the U.S. and below 4% in most major economies.

CPI as of 12/2023, except Japan as of 11/23.

Other Insights

- India, newly the most populous country, is poised for a long period of rapid economic growth. While valuations and regulatory transparency are not particularly favorable, this could be an example of a market that is expected to become increasingly important in global markets.

- China is at its lowest weight in the Emerging Markets index since A-shares became available after a series of economic and regulatory disappointments, yet it remains the world’s second largest economy. This disparity suggests its potential in a portfolio.

- Artificial Intelligence is becoming more mainstream as it is incorporated into more applications and products, which may benefit more companies beyond the “Magnificent 7” in the future.

- Inflation fell despite the headwinds of a 4.6% decline in the dollar over the fourth quarter, adding credibility to inflation progress since imports in commodities prices rise when dollar falls.

- Bitcoin ETFs are here. Unlike predecessors, these would accurately track spot prices through direct ownership of bitcoin, and therefore potentially be suitable in a portfolio. Much of the recent surge (>50%) in bitcoin price can be attributed to anticipated demand from the new ETFs. Should these ETFs become a significant holding among investors, there may be a new risk and return dynamic for bitcoin. Therefore, it is important not to extrapolate recent past performance into the future.

The Legacy of Harry Markowitz

Last year marked the passing of Harry Markowitz. Markowitz won the Nobel Prize in Economics in 1990, though he published his thesis on portfolio optimization in 1952. This lag of nearly 40 years reflects a difficulty in understanding investment science to this day.

Markowitz gave us a framework to make the best use of the available investments, but was explicit that doing so was a tradeoff between risk and return. He understood deeply that there is no best investment or best portfolio, though there can be a most optimal portfolio for a certain investor’s goals. This combines the two parts of optimality: suitability and efficiency. A concentrated portfolio of tech stocks may or may not be efficient, but is clearly not the right fit for most investors’ goals. The appeal of improved performance through efficiency is clear, but providing a portfolio most suitable for an investor’s goal is equally important. Any discussion of the desirability of a stock or a fund without considering how it contributes to an investor’s goal is overlooking Markowitz’s gift. His gift is a holistic understanding on the portfolio, a philosophy that everything matters, and a framework to put it all together.

Markowitz shows us that investing is more like sailing than alchemy — we can’t go faster than the winds of the economy allow, but must find a path that quickly and safely gets us to our destination. Investors use markets to capture the unpredictable but perpetual winds of the global economy and can only work with the returns available.

DISCLOSURES: Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal.