Thoughts on Investing in Extreme Volatility

In the midst of periods of extreme volatility as we have recently experienced, investors may want to remember some fundamental investment axioms:

- The performance of actual investor portfolios is generally not well represented by equity indices.

- A well-defined long-term investment program can help withstand short-term volatility.

- Historically, markets recover after periods of volatility.

- Effective diversification is the single most important portfolio management principle for managing unforecastable risk.

The Performance of Actual Investor Portfolios is Not Well Represented by Major Equity Indices

While headlines in times of market volatility tend to focus on major indices like the S&P 500 and the Dow, it’s important to remember that your clients are typically invested in diversified portfolios representing multiple asset classes. A useful focus may be to consider the New Frontier index that best reflects a client’s systematic risk level for meeting long-term invest objectives.

The graph below tracks the performance of three New Frontier indices: conservative NFGII (20/80 stock/bond; white), balanced systematic risk NFGBI (60/40; yellow), and optimized global risk NFGEI (all equity; green). The S&P 500 (purple) and the DJIA (red) are also displayed. The period is February 24, 2020 to market close on March 9, 2020.

The data show that New Frontier multi-asset diversified optimized indices that include many asset classes relative to targeted systematic risk levels provided valuable managed risk performance during this high volatility period. Globally diversified systematic risk-targeted indices outperformed highly publicized domestic indices.

Performance of New Frontier Indices Compared to S&P 500 (GSPC) and DJIA:

Market Open 2/24/20 - Close 3/9/20

Source: Bloomberg

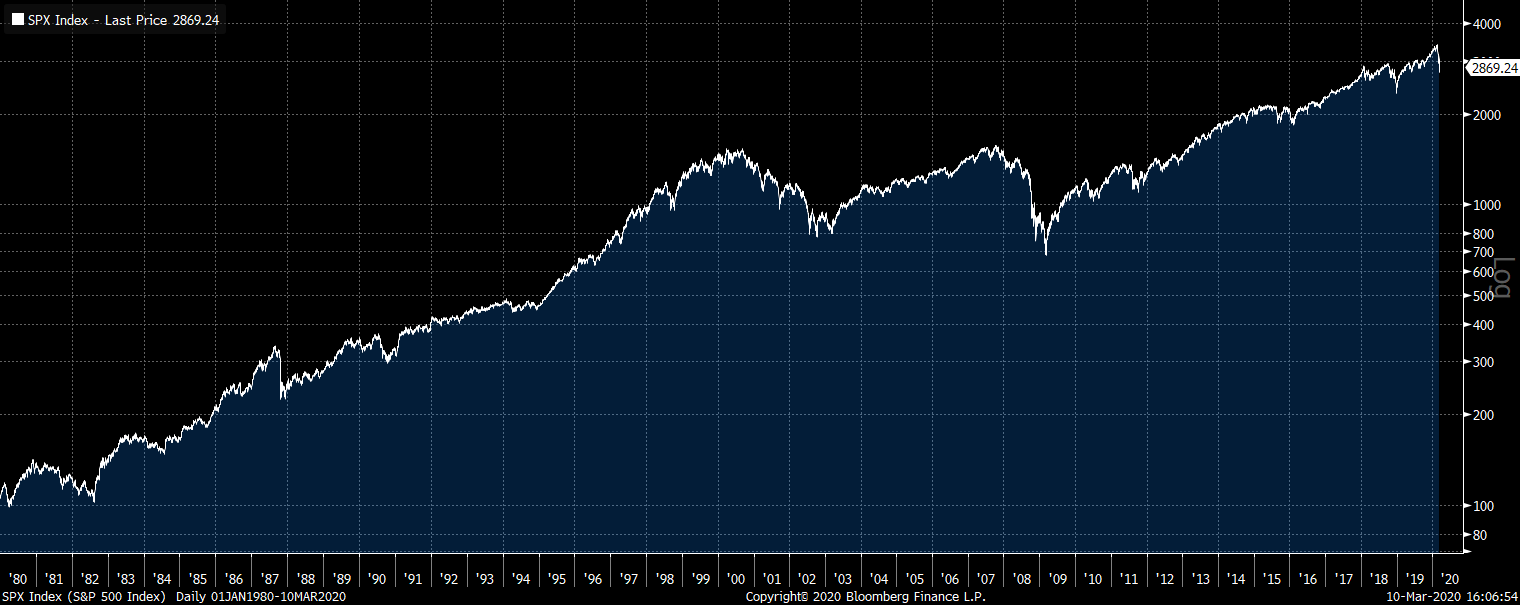

Zooming Out Over Longer Periods

Of course, short term performance does not tell a very reliable story. For long-term investors with retirement and legacy objectives, a longer period can provide a valuable perspective on volatile periods. The graph below of the history of the S&P 500 provides welcome context. A recent article in the New York Times provides some additional insight on the current market downturn.

S&P 500 Over the Last 40 Years (1980-2020)

Source: Bloomberg

Historically, Markets Tend to Recover After Periods of Volatility

It is often tempting to “go to cash” when volatility hits and try to avoid further loss of capital. But once volatility spikes, it’s often too late. We provide below a simple empirical examination of market return and risk following a volatility spike. The data shows that, historically, future returns average higher than usual, but are still quite risky. This means that exiting the market has resulted in lost returns on average, but also there is no “free lunch.”

S&P 500 Returns Following Observed Values of the CBOE VIX: January 1990 - February 2020

| When the VIX is: | 0-20 | 20-25 | 25-30 | 30+ |

| Average 5-day return | 0.14% | 0.09% | 0.28% | 0.47% |

| Standard Deviation (Annualized) | 10.91% | 17.48% | 19.88% | 33.43% |

| Average 1-month return | 0.63% | 0.32% | 1.08% | 1.82% |

| Standard Deviation (Annualized) | 10.75% | 17.31% | 18.76% | 26.95% |

| Average 3-month return | 1.94% | 0.89% | 3.11% | 5.85% |

| Standard Deviation (Annualized) | 11.08% | 17.86% | 16.50% | 22.36% |

| Number of observations | 4372 | 1411 | 655 | 580 |

Sources: CBOE and S&P

A Note of Reassurance

Our Global Multi-Asset ETF portfolios are designed to provide enhanced robust diversification and risk management across many market environments. New Frontier’s investment process uses multi-patented optimization methods to engineer robust solutions over thousands of market scenarios. Our innovations in asset management technology include continuous monitoring and management to maintain optimal exposure to long-term systematic risk objectives.

Volatility and uncertainty are unavoidable facts of financial markets, and the financial impact of the coronavirus has been a sharp reminder of that. Effective diversification remains the single most important portfolio investment principle for mitigating and managing unforecastable risk.

Disclosures: New Frontier Advisors LLC (“New Frontier”) is a federally registered investment adviser based in Boston, MA. The information discussed here is for information purposes only. It does not constitute an offer or solicitation of securities or investment services or an endorsement thereof in any jurisdiction or in any circumstance in which such offer or solicitation is unlawful or not authorized. None of the information contained in this report constitutes, or is intended to constitute, a recommendation of any particular security or trading strategy or a determination by New Frontier that any security or trading strategy is suitable for any specific person. To the extent any of the information contained herein may be deemed to be investment advice, such information is impersonal and is not tailored to the investment needs of any specific person. The data provided is from sources believed to be reliable but have not been independently verified.

Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal. The New Frontier indices are not investable securities. Any investable security would have performance reduced by fees and expenses. In any case, past performance does not guarantee future results. These materials are intended for use by investment professionals only. Any further distribution must comply with your firm’s guidelines and applicable rules and regulations, including Rule 206(4)-1 under the Investment Advisers Act of 1940.

comments powered by Disqus

Need more information?

Contact us to find out how we can work with you.