Q1 2022 Market Perspectives: "Tug of War"

An unusually strong tug of war between economic forces is playing out in global markets, with a booming economy and low unemployment offset by the effects of the Russian invasion of Ukraine and expanded inflation. Expectations over the timing and magnitude of Fed interest rate increases rapidly evolved as clarity began to emerge around central bank responses to inflation. Markets took these events as a potential start of a new investment regime, which resulted in a bad quarter for global stock markets and a terrible quarter for bonds.

Market Performance

Following a surprisingly good 2021, the first quarter of 2022 faced challenges on multiple fronts. 2-year U.S. Treasury yield, most sensitive to interest rate policy, rose to 2.3% by 160 bps during the quarter, resulting in a partially inverted yield curve.

Two key factors that have greatly contributed to market volatility: unknowns around how high rates need to be raised to tame inflation without causing a recession, and uncertainty about how many rate hikes will actually be realized. Against the backdrop of uncertain rates, U.S. bond markets experienced the worst quarter since 1980 with a loss of 6%, while global equities went down 5.4%. Large-cap stocks outperformed small-cap by more than 2%, and U.S. markets continued to lead international markets, though to a lesser extent, with S&P 500 down 4.6%. Value outpaced growth in Q1, supported by energy and less rate-sensitive sectors.

Strategy Performance

New Frontier’s ETF portfolios closed the quarter with negative returns, consistent with broad markets. Stressed bond markets sent conservative portfolio returns close to aggressive portfolios during the quarter.

New Frontier Global Core and Tax-Sensitive portfolios performed in line, while Multi-Asset Income (MAI) portfolios held up relatively better, helped by dividend focused equities that outperformed other market segments. MAI portfolios provide consistent yields of roughly 3.5% - 4%, about twice the yields on broad equity and fixed income markets.

Performance Attribution

Major asset classes were challenged across the board against an increasingly uncertain global backdrop. The overall fixed income exposure weighed on performance, as any fixed income risk taken other than 3-month T-bill didn’t pay off this quarter. While long-duration bonds were the biggest detractors this quarter, their short-term correlation with stocks remains negative, reducing the total risk for our multi-asset portfolios compared to broad markets. Treasury Inflation-Protected Securities (TIPS) benefited from higher inflation, but were overall lower due to rising yields. Within equities, growth stocks and European equities detracted from portfolio performance.

The energy sector (+38%) was responsible for much of equity gains this quarter. Large-cap value stocks, Canadian equities and High Dividends (for MAI portfolios) were the main equity contributors to performance. Canada, a single-country allocation filling a gap in international exposure, was largely supported by commodity exporting amid surging commodity prices. Gold was one of the best performing assets in Q1 amidst macroeconomic uncertainties, providing additional returns and stability for portfolios. Another diversifying asset class benefiting from the inflationary environment was global infrastructure for MAI portfolios, which further enhanced returns and yields.

Market Insights

Surprisingly, in a quarter with major geopolitical turmoil, Fed policy was the emergent risk factor in multi-asset portfolios. The volatile quarter could be broadly characterized as a 2 or 3 standard deviation down event for bonds and a 1 standard deviation down event for equities. Equities markets quickly recovered from the Russian invasion but were left with moderate losses from lowered expectations for economic growth due to the Fed. However, the most dramatic effect of Fed action was the historic rise in interest rates and broad selloff in bonds of all types. Importantly, fixed income volatility remains high. This is indicative of the fundamental uncertainty of whether inflation can be lowered without a serious recession. Should all not go as planned, the Fed may be forced to change course and further impact bond markets.

Markets have largely shrugged off concerns related to the pandemic. Gone are the days when there was a visible relationship between COVID case counts and market returns in a country. It remains to be seen whether the indifferent attitude is a thoughtful reduction of expected disruption, or merely tired ambivalence.

Global Politics

The Russian invasion has had little direct effect on global portfolios. Russia represents close to 2% of global GDP, but was less than 1% of the global stock market before the invasion, so global investors were little affected by the closure of the Russian stock market. The same could not be said for Russian investors who saw spectacular losses in stock, bond and currency—with a closed stock market, interest rates more than doubling to 20%, and the ruble falling over 20%. The subsequent recovery of the propped-up ruble and partial reopening of the Moscow Exchange mean little for global investors as Russian stocks and bonds will remain out of major indices and investment products until well after the current situation is resolved. Russia is economically harming itself and its own people more than the rest of the world.

Meanwhile China remains an area of concern. It has not taken a hard line against Russia, but has also not been willing to alienate the much larger economic community for political purposes either. Some suggest Taiwan may end up being more secure in its independence if the international community continues to express solidarity. China is no less dependent on foreign trade than Russia, and gone are the days of imperialism as an economic benefit. One unrelated positive development for China is the announcement that some of last year’s regulations on the technology industry and U.S. listed Chinese companies will be lessened. While this isn’t in itself enough to fully restore confidence in a market supportive of foreign investors, it’s an important step.

The Economy and Interest Rates

Inflation dominates the thoughts of economists and investors with concerns of direct wealth erosion and economic disruption, as well as the danger of indirectly causing a recession being brought on by Fed actions. Through wealth erosion, inflation presents a dilemma to conservative investors—suffer significant losses in real terms, or take on volatility to preserve purchasing power. While most obvious for investors in cash, inflation-adjusted investment goals are important for all investors.

The Fed has strongly signaled its intention to raise interest rates to fight inflation. It has further indicated that the economy is strong enough that inflation can be lowered to target levels with minimal economic damage. There’s reason to believe that Fed action, and the subsequent results will be different from the 70s, since the Fed’s current reputation for effective economic intervention is much higher than fifty years ago, with the world then fresh off the gold standard and inflation expectations psychologically entrenched. Much of the current inflation can be attributed to unfortunate geopolitical events, and responsibility to solve the problem lies with the Fed rather than with divided politicians. However, the current expected eight rate hikes this year may be disrupted if consumption slows or supply manages to increase. To take the example of oil, high prices simultaneously slow the economy while directly contributing to inflation. [Alternative: both of these are fully possible through another lockdown or the resolution of the Russian invasion].

Anticipated Fed rate hikes have had the predicted effect of raising short term rates (i.e. 1-3 year), but also important is the accelerated unwinding of long dated treasurys and mortgages still on the balance sheet from quantitative easing policies. Thus far, there has been little clear impact on long term rates (i.e. 20+ years). For long duration bonds, this could indicate volatility ahead. Whereas a continuation of short-term volatility would be mathematically difficult since short term rates derive most of their volatility through changes in Fed policy. So, while volatility tends to be persistent, a downward trend toward more moderate levels is likely as the Fed will eventually have to settle on a set of actions.

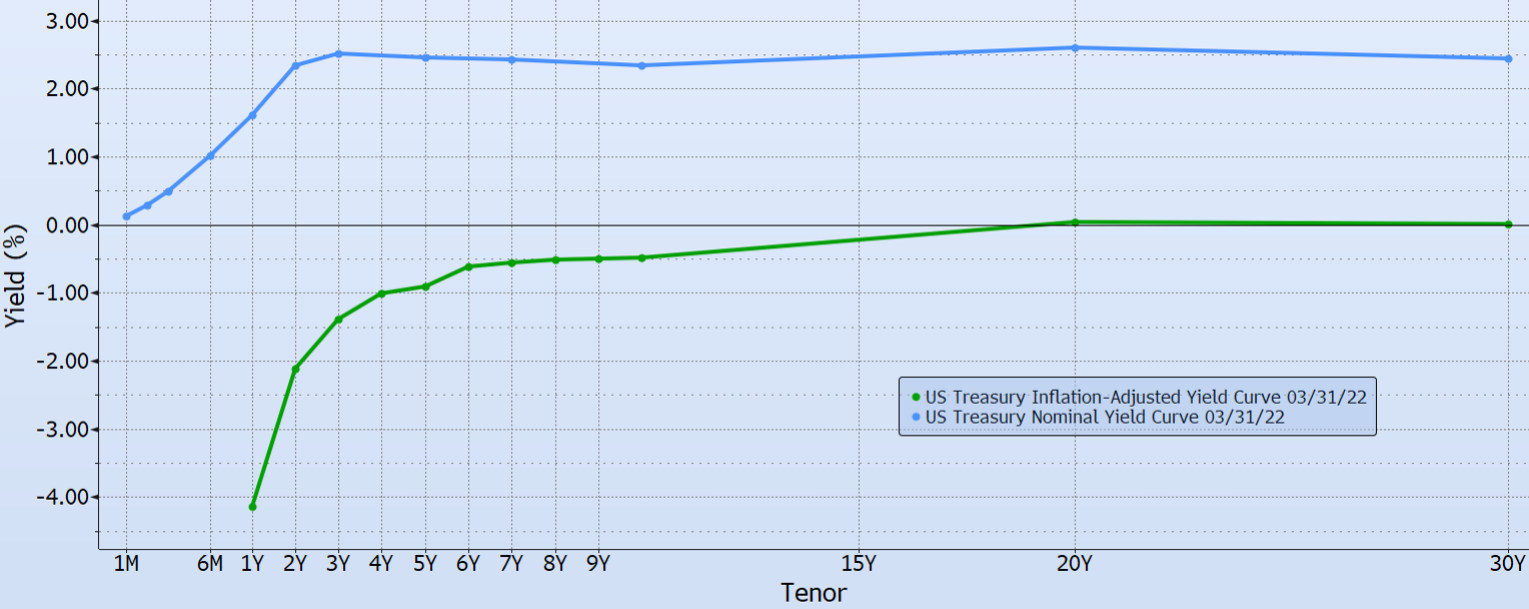

The inverted yield curve is the curious result of the anticipated Fed actions. Despite several historical examples, there’s no credible causal explanation of the relationship between an inverted yield curve and future recession. Intuitively, there’s no economic significance between small differences in either direction between rates, and there’s no statistical significance to a yield curve that’s inverted by the equivalent of a day’s volatility. Additionally, in real terms, the yield curve is not inverted and rises steeply as shown below:

Yield Curve

Source: Bloomberg

ETF Insights on Taxes and Commodities

Tax season reminds us of a major advantage of ETFs over mutual funds and individual security ownership. Tax efficiency is one of the driving forces behind the trend of converting mutual funds to ETFs, and this quarter saw JP Morgan and other large and small investment firms do so. Vanguard was sued by investors in its target date funds for high tax distributions. According to Morningstar, these averaged 12.1% across funds. This problem isn’t confined to Vanguard, since many other target date mutual funds also incurred high capital gains taxes in 2021 (e.g. JP Morgan SmartRetirement funds averaged 10.2% capital gains distributions). This contrasts to New Frontier ETF portfolios which had from 0 to 0.01% capital gains distributions in 2021 across all portfolios.

Since commodities were one of the few asset classes benefitting from recent inflationary events, commodity ETFs deserve a mention. Commodity investing has two main challenges—determining what commodities should be in the investment basket, and how one should invest in those commodities. First, commodity indices vary wildly and frequently suffer from the backtest bias of weighting those with the highest past return most heavily (e.g. over 50% invested in oil). Second, other than precious metals, commodity ETFs generally invest through futures contracts which can distort the exposure to the actual commodity (bitcoin ETFs generally invest in futures as well). Issues such as K-1 taxable distributions, contango (futures price of a commodity is higher than the spot price), ETN (exchange-traded note) counter party risk, and no income mean many commodity ETPs (exchange-traded products) are not recommended investments.

Conclusions and a Look Ahead

Whether or not the economy enters a recession in the next 12-24 months, interest rates and even short lived inflation will present a different market environment than we have encountered before. The current environment features a strong demand-driven economy, low unemployment, manageable volatility, and interest rates closer to their “natural rate.” An optimistic outlook for markets can be made from these observations with sustainable, albeit modest, returns from both stocks and bonds in a multi-asset portfolio. Long term, markets will benefit if the Fed manages inflation well.

Deglobalization further supports the need for thoughtfully diversified multi-asset portfolios. Optimized diversification reduced portfolio volatility even as markets meandered lower this quarter. Economic equilibrium is like tug of war. But market forces are currently pulling much harder than normal and two rockets balanced on a rope should be observed with caution.

DISCLOSURES: Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal.