Q2 2021: "Returning to Normal?"

By

John McCrary, and Dr. David Esch

As the global economy continued to reopen and the recovery gained speed, markets reached new highs. Inflation rose significantly, but prospects dimmed for a sizable infrastructure bill. Thus, some major trends from the first quarter reversed: bond yields fell and value stocks underperformed as the Fed tried to rein in inflation expectations. Despite some mixed signals from the U.S. labor market, the future seems bright for the global economy, although the recovery depends on sustained government support and more equal vaccine distribution.

New Frontier Global and U.S. Index Performance

All New Frontier strategies reached new highs during the quarter. The New Frontier Global (60/40) Institutional Index (NFGBI) returned 5.3% in Q2 and 7.0% year-to-date, as calculated by S&P Dow Jones Indices. Similarly, the New Frontier U.S. (60/40) Institutional Index (NFDBI) returned 5.4% and 8.5% on the quarter and year, respectively. Both 60/40 strategies outperformed their benchmarks in Q2, by 1.0% and 0.4%, respectively.1

New Frontier’s all-equity strategies also performed strongly. The New Frontier Global Equity Index (NFGEI) rose 6.7% in Q2 and 13.1% year-to-date, while the ACWI IMI returned 7.2% on the quarter and 12.7% on the year. Finally, the New Frontier U.S. Equity Index (NFDEI) returned 7.4% and 14.9% this quarter and year, while the S&P 500 NR rose 8.4% and 15.0%, respectively.

Market Performance

The post-pandemic stock rally continued in Q2, reflecting the successful reopening of the U.S. economy. The S&P 500 returned 8.5%, and the NASDAQ returned 9.7%, both reaching all-time highs. In contrast to the first quarter, U.S. growth stocks outperformed value stocks by 6.9%, and large caps outperformed small caps by 4.3% as bond yields fell.2 After a historically bad quarter for bonds, the AGG returned 1.8% in Q2 and credit spreads remained tight. Gold also rebounded, rising 3.6%.

But some trends from the first quarter continued. U.S. equities outperformed international ones by 2.9%, and Chinese equities underperformed the U.S. by 6.2%.3 Real estate was the best performing sector in the U.S., yet international REITs had modest returns, indicating the uncertainty surrounding the international recovery.

Several Unexpected Shifts

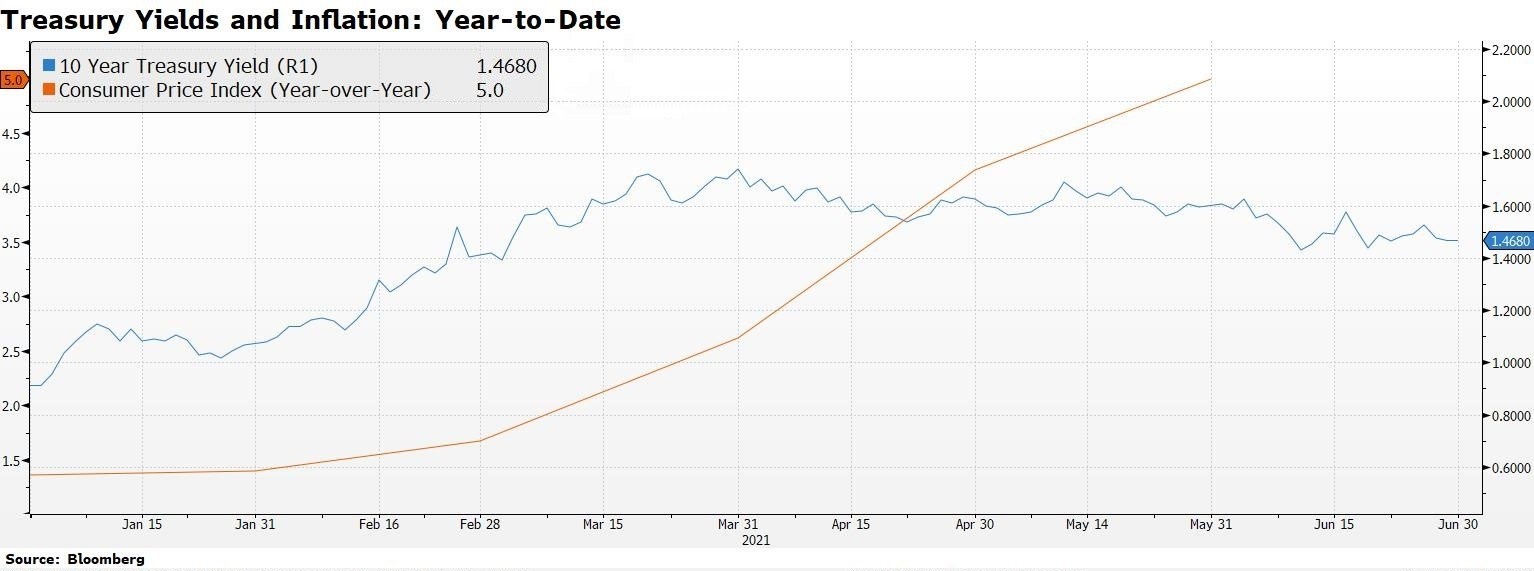

Most investors had expected yields to continue rising, yet 10-year Treasury yields fell by 0.3% in Q2, and inflation readings were considerably higher than expected. Likewise, few predicted higher inflation to be accompanied by lower yields, but the Fed has kept inflation expectations at bay. There were also noteworthy shifts in the U.S. labor market and politics.

Figure 1: The chart illustrates that as inflation rose in Q2, 10-year yields declined unexpectedly.

The Main Themes of the Quarter

Inflation and Investing

Although the Consumer Price Index (CPI) swelled by 5.0% in May, investors should not panic. The Fed’s preferred measure of inflation, which excludes energy prices, was up only 3.4%.4 Much of the rise was due to supply bottlenecks and the resumption of pre-pandemic economic activities. Bottlenecks are usually temporary, and the normalization of consumer behavior should not cause persistent price increases.

New Frontier’s portfolios are nevertheless well-positioned for navigating an inflationary environment. Our portfolios are optimized over many investment scenarios, including ones where inflation is high, and we invest in gold and inflation-protected bonds. If bond prices fell in response to a prolonged period of inflation, bonds would still help maintain the risk control of a portfolio by serving as a hedge against potential stock declines.

The Fed’s Balancing Act

In response to the high inflation readings, critics have argued the Fed should raise rates by 2023 and begin tapering its bond purchases. Yet unemployment stood at 5.9% in June—2.4% above pre-pandemic levels.5 Fed Chair Powell has insisted that inflation will moderate and monetary support will not be withdrawn soon. Nonetheless, Powell also signaled that the Fed may begin tapering if inflation persists.

The Fed has endeavored to both control inflation expectations and continue underwriting the recovery. Powell wants to avoid a repeat of the 1970s when high inflation expectations became self-fulfilling. Instead of raising rates or tapering, Powell’s strategy has been to assure the public that the Fed will intervene if inflation remains high. Investors have believed this message, and bond markets indicate long-term inflation levels close to 2%. Nevertheless, if inflation does not soon subside, the Fed’s stance will be tested, revealing how much inflation it will tolerate to sustain the recovery.

The U.S. Labor Market

Unemployment fell by just 0.1% this quarter despite a steady increase in hiring and a record number of job vacancies.6 Most of the previous decline in unemployment was due to temporarily unemployed workers returning to their jobs. With few temporarily unemployed workers remaining, the unemployment rate can no longer decline as quickly. Moreover, workers laid off due to structural economic changes, for example in ecommerce, are not always well-suited for job vacancies. But overall, the labor market recovery is on course. The Fed projects unemployment will stand at 4.5% in Q4.7

Biden’s Legislative Efforts

Following a productive first quarter, the Biden administration’s only significant legislative achievement in Q2 was a $250 billion bipartisan industrial policy bill. Aimed at increasing the competitiveness of the U.S. relative to China, the bill provides funding for R&D in advanced technologies. Although the government does not always allocate capital efficiently, some prominent economists view the bill as a “down payment” on innovation that should boost long-term growth.8 Biden’s other legislative ambitions have faced considerable resistance in Congress, with negotiations over an infrastructure package continuing.

Other Notable Themes

Continued Global Divergence

While the end of the pandemic is in sight in the U.S. and Europe, many countries—especially developing ones—have limited protection against future waves of COVID-19. Unequal access to vaccines could dampen the global recovery and facilitate the development of new virus variants. More equal vaccine distribution would promote a less uneven global recovery.

Global Taxation

In a victory for Treasury Secretary Yellen, the G7 agreed in June to a global minimum corporate tax rate of at least 15%. 130 countries now support the proposal. Many corporations have long engaged in tax arbitrage, claiming their profits were generated in countries with low corporate tax rates, such as Ireland or Singapore. The OECD estimates that tax arbitrage costs governments at least $100 billion annually in tax revenue.9 Many technology companies face effective tax rates below 15%, so their stock returns may be slightly lower if the G7 proposal is adopted. But the proposal may be good in the long-term if it reduces the amount of resources dedicated to tax arbitrage.

Looking Ahead

This quarter demonstrated that investors should not be confident about their forecasts, especially for inflation and yields. Although prospects for the global economy seem strong, economic recoveries involve unpredictable shifts in economic equilibriums which can cause disruptions, as we have seen with basic shortages in lumber and semiconductors. Given we do not know what disruptions to expect later this year, an optimally diversified portfolio remains essential.

Research Update

On May 13, 2021, Professor Antoinette Schoar presented the fourth of the Boston CFA Distinguished Lecture Series, sponsored by New Frontier. Dr. Schoar is the Stewart C. Myers-Horn Family Professor of Finance and Entrepreneurship at the MIT Sloan School of Management, and one of the world's leading scholars on cryptocurrencies. The title of the lecture was “Who Owns and Trades Bitcoin: Evidence from the Blockchain.”

Dr. Schoar’s presentation was aimed at curious investment professionals who may not already be experts in blockchain technology. She started with three popular narratives about Bitcoin and proceeded to debunk them, leaving only one possibility. What follows is a brief summary of Dr. Schoar’s comments and critiques on each of these three purported uses of Bitcoin:

- A Vehicle for Monetary Transactions

Ten to fifteen minutes is the median time for bitcoin transactions to clear and become visible on the blockchain, the official ledger of Bitcoin transaction, according to Professor Schoar. A credit card, by comparison, can clear such transactions nearly instantaneously. Secondly, the rewards, in coins, for mining activities which effectively do the work of clearing the transaction and updating the ledger will disappear once the limit of bitcoins has been reached, and owners of bitcoins will have to pay an additional fee to process transactions. Thirdly, the activity of transacting coins, including mining operations, is tremendously inefficient and consumes a sizable portion of global energy consumption, far more than more traditional currencies. This level of consumption is unsustainable, especially if cryptocurrencies were to replace traditional currencies and scale up accordingly in volume. For these three reasons Bitcoin is too slow and inefficient to function effectively as a payment mechanism.

- A Store of Value

Bitcoin is far too volatile to function as a store of value for ordinary investors. A few individuals own most of the coins in existence, and they can easily manipulate the exchange rate between dollars and coins to suit their purposes. Bitcoin is also subject to a high degree of price impact, making it far less suitable for ordinary investors as a store of value than, for example, the U.S. dollar, the Euro, or even gold.

- A Speculative Investment

In Professor Schoar’s expert argument, this is the only remaining narrative by process of elimination. Bitcoins do not represent an investable asset class with a stable risk premium, which is a necessary feature for inclusion in non-speculative portfolios like retirement funds or individual investment accounts.

Dr. Schoar’s focused and clear arguments perfectly illustrate why Bitcoin, and by extension cryptocurrencies, are not suitable vehicles for risk-managed investment products such as New Frontier’s. They are not suitable vehicles for retirement or estate accounts. While not excluding the possibility of improving some of these issues through future innovations, or finding other applications for blockchain technology, these clear explanations are well aligned with our thinking about Bitcoin, and give a precise argument as to why we don’t consider it an investable asset class.

DISCLOSURES: Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal.

References

1NFGBI’s benchmark is a blend of 60% ACWI IMI and 40% 3-month T-Bills. NFDBI’s benchmark is a blend of 60% S&P 500 NR and 40% T-Bills.

2These comparisons are based upon the S&P 500 Value and Growth indices, the Russell 2000 Index, and the S&P 500 Index. Also, note that yields on short-duration Treasurys actually rose.

3Comparisons are based upon the ACWI ex-US Index, the MSCI China Index, and the S&P 500 Index.

4Federal Reserve Economic Data. “Consumer Price Index for All Urban Consumers.” Updated monthly, https://fred.stlouisfed.org/series/CPIAUCSL.

Federal Reserve Economic Data. “Personal Consumption Expenditures Excluding Food and Energy.” Updated monthly, https://fred.stlouisfed.org/series/PCEPILFE.

5Federal Reserve Economic Data. “Unemployment Rate.” Updated monthly, https://fred.stlouisfed.org/series/UNRATE.

6Federal Reserve Economic Data. “All Employees, Total Nonfarm.” Updated monthly, https://fred.stlouisfed.org/series/PAYEMS.

Federal Reserve Economic Data. “Job Openings: Total Nonfarm.” Updated monthly, https://fred.stlouisfed.org/series/JTSJOL.

7Federal Open Market Committee." June 16, 2021: FOMC Projections materials." June 16, 2021, https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20210616.htm.

8Glanzman, Adam." Senate Approves $250 Billion Bill to Boost Tech Research." The Wall Street Journal, June 8, 2021, https://www.wsj.com/articles/senate-approves-250-billion-bill-to-boost-tech-research-11623192584.

The Economist. “Congress is set to make a down-payment on innovation in America.” June 5, 2021, https://www.economist.com/united-states/2021/06/05/congress-is-set-to-make-a-down-payment-on-innovation-in-america.

9Hannon, Paul and Kate Davidson. "G7 backs Biden's sweeping overhaul of global tax system." The Wall Street Journal, July 1, 2021, https://www.wsj.com/articles/u-s-wins-international-backing-for-global-minimum-tax-11625153698.