Don't Underestimate the Role of Long-Term Treasurys in Your Portfolio

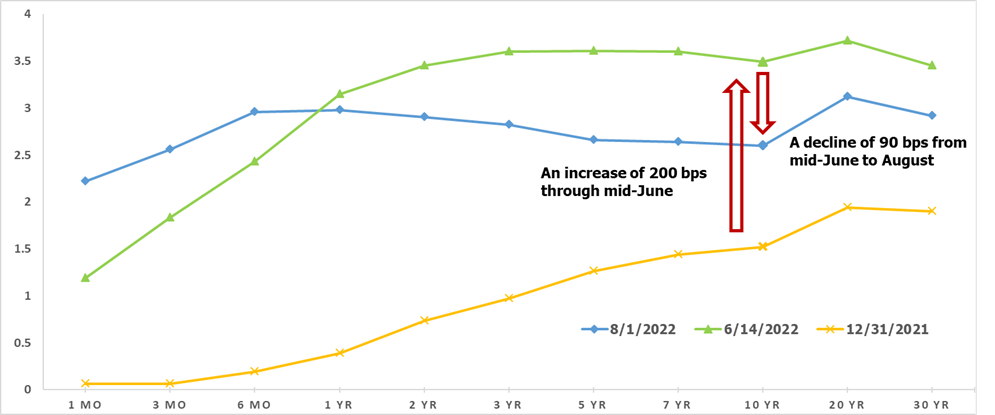

Bond investing has been challenging in 2022 due to historic macroeconomic events and significant interest rate hikes by the US Fed. The velocity of the yield change YTD has been stark, as illustrated below. For example, after an increase of nearly 200 bps through mid-June - with 10-year Treasury yields reaching 3.49% on June 14th - long-term yields declined by 90 bps in just thirty-three trading days to land at 2.6% as of the beginning of August.

Despite the unsettling volatility and rising yields, investors must keep in mind the multi-faceted role that long-term Treasurys play in a balanced 60/40 investment portfolio. To fully understand the impact of Treasurys requires looking beyond simple yields, and taking a more holistic look at long-term Treasurys and their distinct benefits in an optimized portfolio, including:

Value retention – acting as a more stable shock absorber during equity declines,

Volatility dampener - mitigating portfolio risk,

Return premium with little to no credit risk.

That said, as long-term Treasurys have declined this year, many investors question the role they play in their portfolio. Nevertheless, long-term Treasurys have proven themselves invaluable in a portfolio repeatedly over time, especially during periods of unforeseen market dislocation and volatility. Below we discuss the benefits of holding long-term Treasurys at the total portfolio level - compared to short- and intermediate-term Treasurys - examining the risk/return characteristics of each in greater detail and how we see long-Treasurys helping to optimize portfolios - even in today’s rising rate environment.

US Treasury Yield Curve – The velocity of the 10-year yield change YTD has been stark

Source: U.S. DEPARTMENT OF THE TREASURY

What Drives the Value of Long-Term Treasurys?

Long-term yields reflect the market's expectation of future rates plus a premium. Many argue the premium represents the compensation that risk-averse investors demand for bearing risks embedded in long-term bonds.

While dissecting premium and interest rate expectation is not the focus of this blog, it’s important to understand that both are affected by economic uncertainty, including any surprises in monetary policy, inflation, supply and demand, or future growth expectations.

Notably, the more-aggressive-than-expected rate hikes due to inflation shock have contributed significantly to the yield paradigm this year. While the whole yield curve has broadly shifted up with rate increases, long-term yields have occasionally retreated – reflecting investors’ expectations for lower rates in the future.

Further, while bonds have lost value so far this year, it is important to remember that bonds are somewhat self-healing, meaning that a bond’s price eventually returns to par value when held to maturity – to the extent they don’t default. This is even more so for diversified bond funds with a specific duration exposure. So, while rising rates have led to lower share prices, bond funds will have higher income to distribute. Individual bonds within the bond fund will also mature at par and new higher yielding issuers can be purchased at the lower price.

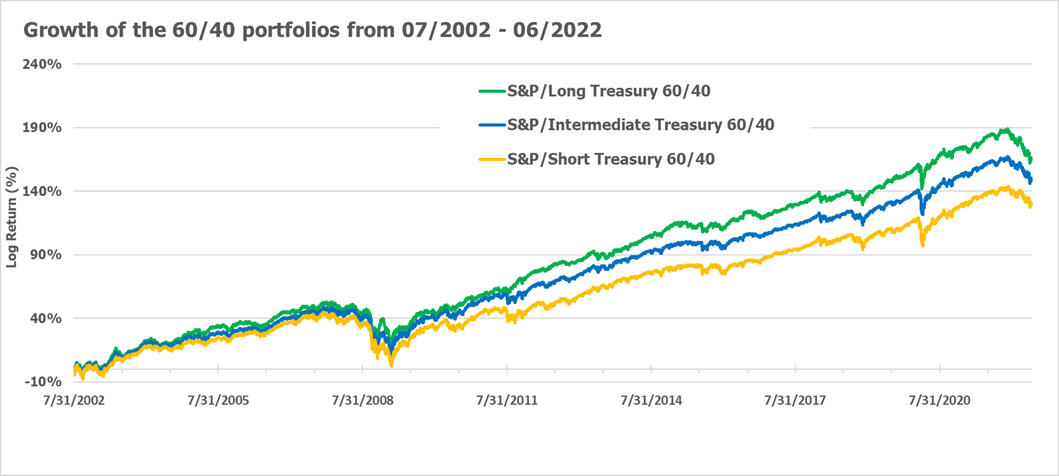

Long-Term Treasurys Provide Excess Historical Return

As illustrated below, investors have been rewarded for holding long-duration exposure in the portfolio for the last two decades. Consider the following three 60/40 balanced portfolios constructed with short, intermediate, and long-term Treasury ETFs, along with S&P 500 – in these portfolios, long-term Treasurys have realized excess returns relative to shorter-term Treasurys, and positively contributed to the risk-adjusted returns.

Sources: Bloomberg ETF daily returns (SPY for S&P 500, TLT for Long Treasurys, IEF for Intermediate Treasurys and SHY for Short Treasurys) from 2002/07/31 (inception date of the Treasurys ETFs) to 2022/06/30 are used to construct the 60/40 portfolios, with a quarterly rebalancing. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS.

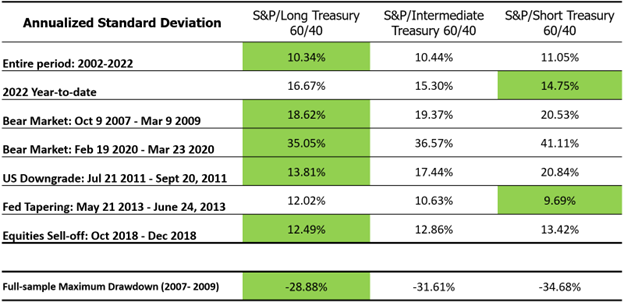

Long-Term Treasurys Help Reduce Portfolio Volatility

The table below illustrates the realized volatility of the three 60/40 portfolios in the specified stressed market periods. Highlighted numbers indicate the highest total return realized during that period. The portfolio with short-term Treasurys performed best in 2013’s taper tantrum and 2022 YTD – periods of extreme, rapid, and unexpected changes to monetary policy. In all other periods, long-term Treasurys have provided relative outperformance that has helped cushion equity drawdowns. It supports the thesis that having long-term Treasurys in the portfolio has helped mitigate the overall portfolio volatility, not only in the long run, but more importantly, during crisis periods when equities have declined dramatically. In terms of risk metrics, the persistent strong negative correlation of long-term Treasurys to equities results in a greater reduction in a portfolios’ total risk, and a greater increase in risk-adjusted return relative to shorter-term Treasurys.

Long Treasurys Stand Tall During Crisis

Sources: Bloomberg ETF daily returns (SPY for S&P 500, TLT for Long Treasurys, IEF for Intermediate Treasurys and SHY for Short Treasurys) from 2002/07/31 to 2022/06/30 are used for constructing the 60/40 portfolios, with a quarterly rebalance schedule. Portfolio standard deviations represent realized daily standard deviations in annualized terms. The highlights indicate the outperformance during the period. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS.

While short-term Treasurys also observe a negative correlation with equities, due to the smaller magnitude of the returns (historical monthly returns range from -1.4% to 1.8% with the average of 0.14%), their overall ability to smooth the fluctuations in the portfolio’s value is limited.

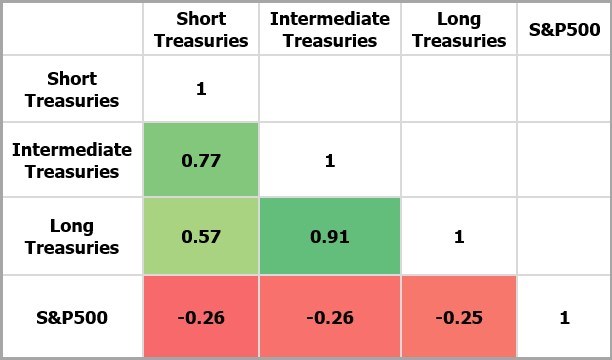

Long Duration Packs More Punch

Source: Bloomberg. Correlations are calculated on ETF monthly returns from 2002/07-2022/06

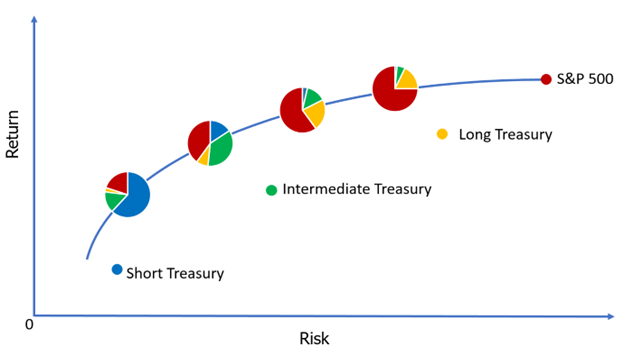

Long-Term Treasurys within the Optimized Portfolio Context

The optimal allocation to long-term Treasurys depends not only on their expectations, but also on the investment objective of the portfolio they’re in. New Frontier believes all assets should be measured in the context of the benefits they add to a portfolio, rather than by their risk-return characteristics in isolation. In an optimized asset allocation, the role of long-term Treasurys is not limited to singularly adding total return as a standalone asset. Rather, it interacts with other assets to reduce overall portfolio risk at each point of the efficient frontier.

Long-term Treasurys, which are typically characterized by greater average returns, high volatility and strong negative correlation with equities, present a “versatile” asset for portfolio optimization. For example, when constructing portfolios along the frontier, a conservative portfolio may hold more shorter-term Treasuries with modest long-duration exposure for risk control. While a more aggressive portfolio may be better served allocating proportionally more of its fixed income exposure to long-term Treasurys for hedging higher equity risk. Optimizing long-term Treasury holdings allows us to reach for alpha in other ways and potentially hold more aggressive equities - without increasing the risk profile of the portfolio as a whole.

The chart below shows a hypothetical mean-variance efficient frontier for portfolios comprised of three Treasury bond ETFs and the S&P 500.The four optimal portfolio allocations on the frontier represent four target risk objectives - stock/bond ratio of 20/80, 40/60, 60/40 and 75/25, respectively. The proportion of long-term Treasurys in the bond allocation shifts higher for more aggressive portfolios even though the weight to bonds decreases overall.

Hypothetical example for illustrative purposes only. ETF return data from 2002/07 to 2022/06

Conclusion

At New Frontier, we optimize portfolios over thousands of potential future scenarios to build a diversified portfolio positioned for an uncertain future. Our long track record has proven the benefits of New Frontier’s strategic approach to investing – we do not rely on directional bets or luck, but maintain optimized, effectively diversified portfolios via our multi-patented investment process. And our portfolios sustain their value through many different market environments.

Building the right portfolio for an investor is not simple – as we’ve shown a riskier bond may lead to a less volatile portfolio. History has shown that attempts to time interest rate changes can often end up as costly mistakes . The future is uncertain and many factors drive interest rates and the near-term prices of Treasurys. But focusing on the portfolio rather than betting on individual assets can lead to better outcomes for investors. Even in today’s landscape with high inflation and volatile interest rates – we see the multi-faceted benefits of long-term Treasurys playing a valuable role in diversifying equity risk and reducing overall portfolio volatility.

Disclosures:

Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal. The indices are not investable securities. Any investable security would have performance reduced by fees and expenses. Any distribution must comply with your firm’s guidelines and applicable rules and regulations, including Rule 206(4)-1 under the Investment Advisers Act of 1940.