Any Time is the Right Time to Start Investing

Due to the fluctuating nature of the economy, present market conditions can prompt investors to wait for a better time to invest, theorizing that waiting until after an economic downturn – whether a recession, government shutdown, or pandemic – will ensure greater return on investment. In reality, waiting for a favorable market scenario leaves investors at a disadvantage compared to those who enter the market irrespective of current conditions.

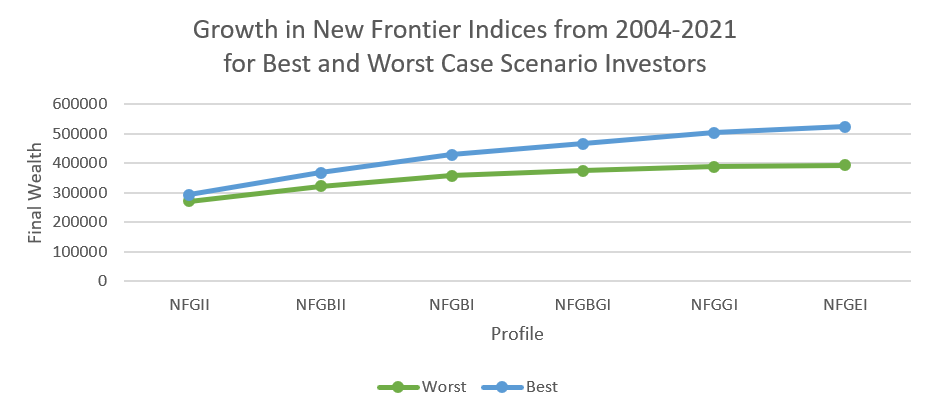

Let’s take a look at two hypothetical outcomes… the “Best Case Scenario” investor, who luckily invested their capital on the best day each year, and the “Worst Case Scenario” investor, who unfortunately invested their capital on the worst day each year. The chart below shows how these investors would have fared in each of New Frontier’s global risk-targeted indices, which track investment activity of our six global core multi-asset portfolios. Indices range from the most conservative profile, New Frontier Global Income Index (NFGII), 20/80 stock/bond ratio, to the most aggressive profile, New Frontier Global Equity Index (NFGEI), 100% equities. Each hypothetical investor contributed $10,000 each year from 2004-2021. Over the years, both “Best” and “Worst Case Scenario” investors saw their initial investment grow.

The most important observation to note is that in all cases, investors saw their initial contribution increase, coming out ahead regardless of when they entered the market. In practice, most investors are going to end up somewhere in the middle of the two outcomes if they stick to their plan. This is a particularly desirable outcome when, for example, you are investing in or looking to establish an income generating portfolio for retirement. The only investors who are truly “losing” are those who are not invested, as it prevents them from realizing any gains whatsoever.

In light of this information investors should strive to invest in a risk-return efficient portfolio that is uniquely designed to deal with uncertainty. New Frontier’s adaptive process is built to accommodate new information on market conditions to rebalance back to optimality, effectively positioning portfolios for weathering any risks that may lie ahead. In addition, New Frontier’s portfolios are:

- Built for the long-term. Our portfolios focus on mitigating risk and achieving gains in the balanced portfolio over long-term horizons. Not betting on any one asset class and investing in global economic growth opportunities as the most reliable source of return helps ensure portfolio longevity.

- Rebalanced via an objective test. Going with one’s gut or trying to speculate on the future is not advisable, and an impossible exercise. That’s why rebalancing portfolios with an objective, statistically rigorous litmus test, like the Michaud-Esch Rebalancing Test is a crucial part of any well-defined asset management program.

- Highly diversified across many factors.All well-constructed strategies have exposure to a wide range of securities to spread risk across asset classes. Notably, a 60/40 portfolio has exposure to a wide range of securities and is called a balanced portfolio for a reason. Not only does it balance the risks of stocks and bonds, but when executed well, it also balances risks across all asset classes.

- Optimized at the core. Michaud Optimization addresses information uncertainty in risk-return estimates. That includes building a sophisticated portfolio with many different ETFs representing a variety of asset classes to eliminate any portfolio inefficiencies so investors get every bit of return possible from their portfolio while avoiding unrequired risk.

To learn more about New Frontier’s risk-return efficient portfolios, and how our adaptive process may benefit you and your clients, contact us at 617-482-1433, or at nfglobal@newfrontieradvisors.com.

Disclosures:

The indices are not investable securities. Any investable security would have performance reduced by fees. Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. The indices are total return indices and the hypothetical $10,000 investments throughout 2004-2021 period assumes reinvestment of dividends and capital gains distributions. Final wealth amounts are as of 10/12/2021.