The US market has not moved much this year. US stocks rebounded strongly in May, but remain largely flat for the year. Meanwhile, international equity returns have been strong, outperforming the US market by over 10% YTD.

International markets are better diversified than the US. The US market continues to be driven by a concentrated group of companies, which are highly sensitive to shifts in sentiment, capital spending, regulation, and competition. International markets are generally less concentrated. Europe, for example, has limited exposure to these large growth stocks and offers a more balanced sector mix. This year, strength in banks and defensive sectors has helped Europe become the top-performing equity market, delivering a 21% return YTD.

Also, rising concerns about the US fiscal deficit, slower growth and trade and tax policy uncertainty have impacted international capital flows with direct implications for asset prices and currency values. In addition to generally rising values of international assets, the dollar has weakened roughly 8% this year, providing a further boost to international assets, including both equities and government bonds.

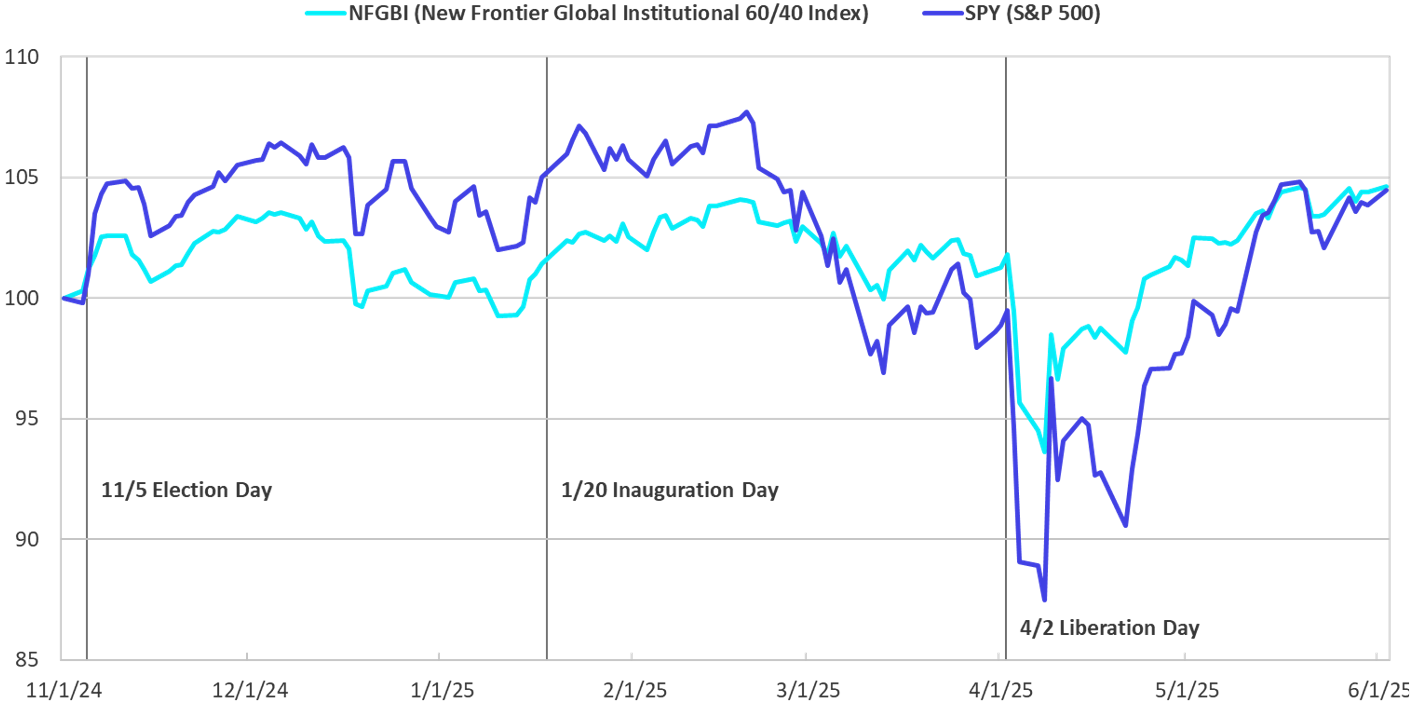

In a world where countries are moving through very different economic and policy regimes, global diversification remains a key approach. It helps reduce concentration risk and provides a smoother investment experience across different environments. Adding exposure to alternatives like gold and including international minimum-volatility equities has further enhanced portfolio resilience this year. As the chart below shows, the global balanced 60/40 portfolio showed greater stability than S&P 500 during tariff-driven volatility.

Price Changes Normalized as of 11/1/2024

Source: Bloomberg

Key Takeaways:

- International equities have outperformed the US by over 10% year-to-date, driven by strength in Europe and supported by a weaker dollar.

- The US market remains concentrated in a few large-cap growth stocks, while international markets offer broader sector exposure.

- Countries are following very different economic and policy paths, making global diversification more important than ever.

- Potential new taxes on foreign investors could lead to greater divergence between US and international markets.

Currency volatility can affect short-term returns, but it has little impact on long-term investment outcomes. This year’s volatility has raised questions about how to think about currency exposure in a global portfolio. The key consideration is whether currency offers a risk premium that aligns with the portfolio’s objective or helps diversify total risk. Unlike stocks or bonds, currencies don’t generate income or cash flows, and exchange rates are driven by inflation or interest rate differences, which can’t move in one direction indefinitely.

The dollar has remained strong for several years, supported by U.S. economic strength, tighter monetary policy, and global demand for dollar assets. This has led to the outperformance of U.S. dollar hedged international equities relative to unhedged counterparts, and of U.S. Treasurys over international bonds. But no currency remains dominant forever. Over time, shifts in inflation, yields, and capital flows tend to bring currencies back toward equilibrium. This year, we have seen that trend reverse.

For these reasons, we do not take active currency risk in our strategic global portfolios or make short-term directional bets. For international equities, currency hedging adds cost, complexity, and taxes, with no improvement on long-term return. In the short term, adding currency exposure to local market returns supports geographic diversification and reflects each country’s broader economic and policy environment. So, we do not actively hedge currency in our global portfolios. On the fixed income side, we maintain dominant allocations to U.S. Treasurys, with only modest exposure to international government bonds, given their lower yields and additional currency risk.

Key Takeaways:

- Currency movements can impact short-term returns, but they do not provide consistent return benefits or meaningful risk management over the long term.

- We do not take active currency risk or hedge currency in our global portfolios.

We don’t chase short-term market moves driven by shifting headlines or speculation.

That includes trades based on tariff news, political policy speculation, or trendy sentiment such as the TACO trades.

While some investors may have benefited from correctly timing policy shifts, this trade depends heavily on market sentiment and timing and is thus risky and unlikely to be sustainable in the long run. The best players in these types of trades have first access to timely information, and by the time the information becomes public, it is no longer profitable.

The safest policy for long-term strategic investors is to not play the game. At New Frontier, we avoid short-term bets and market timing based on sentiment or speculative forecasts—an essential part of our risk management strategy.

Key Takeaway:

- Relying on market timing and sentiment is risky and unsustainable. Our approach focuses on long-term discipline and risk-managed investing.