Key Takeaways

- Deglobalization supports diversification: Reversing global trade reduces economic productivity, but the resulting decoupling of international markets increases the protective value of geographic diversification.

- Oil uncertainty harms the aggregate economy: Even though the U.S. produces as much energy as it consumes, unpredictable price spikes cause consumers to cut spending while producers hoard profits, slowing overall growth.

- AI implementation offers better long-term value than AI infrastructure: The multi-trillion-dollar build-out of data centers carries severe depreciation risk. Long-term returns will likely favor the broad market companies successfully implementing AI rather than the few firms building it.

- The "Conservative Investor's Dilemma": Gold's recent volatility and failure to act as a haven during the Iran conflict proves that traditional defensive assets require strict risk management.

- Intermediate Treasurys are a fixed income sweet spot: They avoids the severe fiscal and inflation risks of the 30-year bond while providing enough yield to hedge against equity downturns.

- Private asset returns are converging with public markets: The flood of capital into private credit and equity will drive the spectacular returns of the past to normalize downward as the illiquidity premium shrinks.

Executive Summary

Deglobalization, a new crisis, and what to ignore

The first quarter of 2026 had two distinct regimes. The first two months continued the theme we laid out to start the year: a decoupling global economy, broad AI implementation, and a widening opportunity set as long-ignored asset classes earned back their premiums. Then the Iran war began, oil prices jumped, and markets did what markets do in a crisis—focused on a single variable and treated everything else as noise.

Correlations are high when investors focus on the same thing, like the outcome of a war. That does not mean the underlying characteristics of the assets have gone away. The structural drivers that produced broad returns in January and February did not disappear in March; they were simply eclipsed. Over any meaningful investment horizon, correlations reemerge and diversification again matters. Tariff uncertainty has been replaced by Middle East uncertainty – different signal, same noise.

Market Performance

The quarter started with asset classes continuing the broadly distributed gains from late 2025 but stock and bond markets abruptly turned downward with the start of the Iran War.

Source: Bloomberg. Asset class return reflects ETF total return.

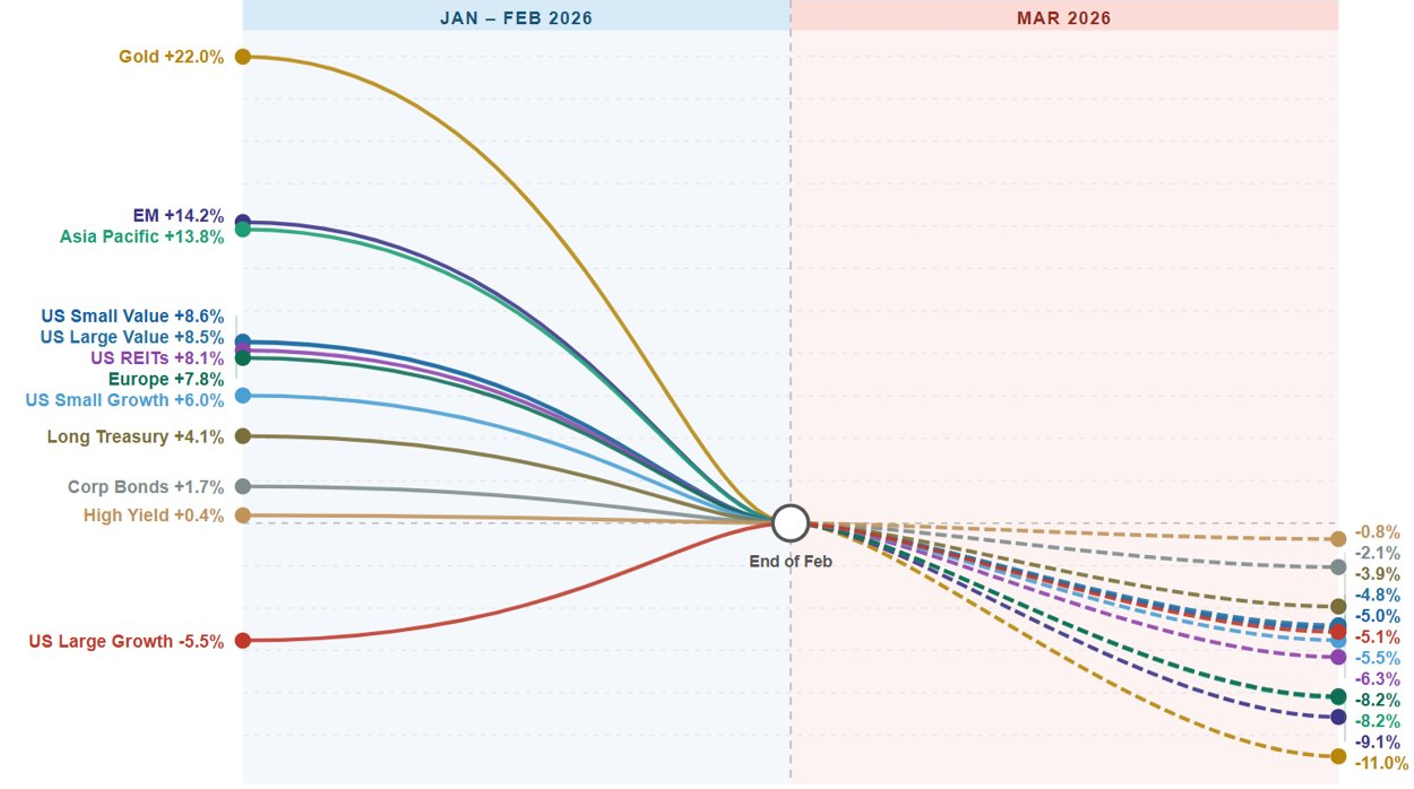

Most asset classes declined in March, coinciding with the Iran War, with international markets underperforming the U.S. during the selloff, as higher oil prices and a stronger U.S. dollar weighed more heavily on energy-sensitive economies. Yet stronger performance earlier in the quarter allowed international equities to finish ahead. Asia Pacific gained 4.5% and emerging markets rose 3.8%, while Europe declined 1%. Overall, ACWI ex-U.S. gained 2.0% for the quarter, compared to a 4.4% decline in the S&P 500.

The weakness in U.S. equities was concentrated in large growth stocks, which declined 10.4%, while value held up well, gaining 3.3%, and small-cap value rose 3.2%. This extended the shift that began late last year, with returns broadening beyond a narrow group of tech stocks. Dividend equities outperformed the broader market by a wide margin. Gold gained a volatile 8.6%, and U.S. REITs also performed well, while international REITs gave back earlier gains during the March drawdown.

Fixed income returns were flat for the quarter but uneven. Early expectations for rate cuts supported duration, but this reversed with the war as inflation concerns pushed yields higher, leaving long-duration Treasuries roughly flat after significant intra-quarter volatility. International bonds and emerging market debt were among the weakest segments, declining around 2% as dollar strength and rising yields reversed earlier gains.

The Economy

For most of the quarter, the underlying economy continued its earlier trajectory: consistent growth, gradually softening labor markets, and inflation plateaued modestly above the Fed’s 2% target. Corporate earnings are strong, and very strong for energy and tech companies (though with some caveats). However, the Iran war changed overall sentiment to interpret the market through the single perspective of oil prices and their implications for inflation.

Deglobalization Continues

We wrote earlier that international markets had stopped moving in lockstep with the U.S. as policies and growth diverged around the world. Countries continue to invest heavily in self-reliance – in energy, defense, manufacturing, and advanced technology. These are inherently expensive and high economic-friction transitions. Sourcing critical minerals outside a dominant supplier, building semiconductor fabrication plants at home rather than in the most efficient location, and maintaining domestic defense manufacturing all mean giving up global economies of scale. The aggregate effect is a less efficient world economy, which all else equal is inflationary and a drag on productivity.

Source: Bloomberg. Correlations calculated using weekly returns of the iShares Core MSCI Europe ETF, iShares Core MSCI Pacific ETF, iShares Core MSCI Emerging Markets ETF, iShares MSCI Emerging Markets ex China ETF, State Street SPDR S&P China ETF, and Vanguard Growth Index Fund ETF.

The implication for international investing is complex. Deglobalization supports the case for international diversification from a risk perspective, because individual markets become less correlated when driven by different policy regimes. The effect on expected returns is more ambiguous. Going back to Adam Smith’s wealth of nations, the concept that specialization and trade make each country’s economy more valuable goes in reverse when countries reshore activity they are not naturally positioned to perform efficiently. For investors, the practical conclusion is that international diversification is more valuable as a risk management tool, while broad return expectations should, on balance, be modestly lower than they were in the prior era. The economies that isolate themselves the most will have the lowest returns while paradoxically require the most capital to make the transformation.

Inflation: Shadow Inflation, Tariffs, and Expectations

Through 2025, we observed that tariffs were not producing the inflationary spike some feared because corporations were absorbing costs into their margins. That buffer is finite. A year into the tariff regime, pre-tariff inventory is gone, supply chains have had time to adjust, and the profit cushion has fallen, which leads to a need for a new price equilibrium in many industries. While still far more modest than initially feared, there is evidence of some price pass-through. The oil shock from the Iran war temporarily took over the inflation story, but the tariff-driven pressure is quietly catching up underneath.

Globally, headline inflation has plateaued in the 2–3% range. For the United States, the combination of tariffs, a weaker dollar, reduced immigration tightening labor markets, and energy price shocks suggest inflation will remain above the Fed’s 2% target. The Fed has not publicly capitulated, but there is a serious possibility that 2% is no longer a realistic target in the near-term. The implications for asset allocation are meaningful: modestly higher nominal yields across the curve, a renewed role for TIPS as an inflation hedge, continued usefulness of real assets like gold and real estate as diversifiers, and caution on long-duration nominal bonds as a standalone hedge. Investors should treat inflation as an underpriced risk, more nuanced than a direct result of energy costs. While the market is focused on oil prices, the more meaningful pressure comes from fiscal policy, tariffs, and the structural inefficiency of a deglobalizing economy.

Oil, the Dollar, and the Cost of Uncertainty

A straightforward view is that the U.S. economy is roughly neutral to oil prices because domestic production is close to domestic consumption. That intuition is right but misleading. Even if the price change is just a manageable reallocation of wealth, the volatility and uncertainty around prices impose an economic cost. Producers who benefit from higher prices tend to bank the windfall rather than invest in new capacity, because the future is too uncertain to justify long-term capital commitments. At the same time, consumers forced to pay more cut back on other spending immediately. Economic losses outweigh gains because uncertainty is asymmetrically harmful – it discourages long-term investment and encourages short-term reductions. The same logic applies to tariffs and to Fed policy. Uncertainty is a tax on long-term capital formation.

While the dollar rose modestly in the first quarter, there is a question about what it means for the U.S. economy. The U.S. plays a (still) highly integral role in the global economy, and the change in the dollar is a complex equilibrium of many forces. In contrast to a small economy, where a currency move revalues the local economy for the rest of the world, when the dollar moves, it partially reprices the world for the entire economy. Commodities, global debt, trade, and central bank reserves are typically denominated in dollars. Since the dollar has implications for nearly all assets, the dollar’s level should not be simply used as a signal about the relative attractiveness of U.S. versus international assets. Furthermore, dollar volatility cannot simply be solved for a U.S. investor with naïve international diversification. But concerns for the dollar are largely overstated. For now, the dollar’s resilience during the Iran war suggests its role in the global financial system remains stable.

The Fed and Interest Rates

The quarter was notable in how little the Fed moved markets. In a year when a presumptive new Chair was named and will likely be confirmed in the coming quarter, one might have expected changing rate expectations. The market continues pricing a gradual path broadly consistent with the Fed’s longstanding guidance, with adjustments driven by economic data. But the market may be complacent. A new Chair with a different perspective could pursue rate cuts more aggressively than current conditions warrant. The result would vary greatly with conditions, but would likely cause a drop in short rates combined with a risk of higher long rates from inflation expectations.

- Competing forces: Intermediate and long rates pulled up between inflation and economic growth risks.

- Rates are correlated: There has been strong correlation between short-term and longer-term rates as both were moved by inflation expectations

- Inflation risk: Significant long-term inflation is not reflected in bond prices. Either the market is heavily weighting deflationary risks from recession, or only lightly weighting inflation risk from sources such as debt, stimulus, and deglobalization.

- Case for Intermediate Treasurys: They would benefit from expectations of prolonged rate cuts while being somewhat insulated from inflation risks. Therefore, they are likely to maintain their equity-risk mitigation character.

- High Yield: Credit spread remains tight while volatility remains low. These could change quickly so it needs to be monitored.

The Conservative Investor’s Dilemma, Revisited

We raised a concern at the start of the year that some historically defensive assets have become less reliable risk management tools. Gold, a trusted diversifier for the better part of two decades, had a volatile rise throughout January and February and then fell in March precisely when conservative investors most needed diversification. A gold that can double in a year can also decline 15% in a month. Gold still has a place in a portfolio due to its unique diversification properties, but investors need to adjust its role in a portfolio.

Long Treasurys, the hedge of past crises, fell with equities in March because the crisis was inflationary rather than deflationary. Minimum volatility equities held up relatively well, but did not fully offset the concentrated drawdown in U.S. growth. Cash yields are drifting lower as the Fed begins to ease. There is no single compelling safe haven right now, and each traditional defensive asset has at least one unusual risk characteristic that it did not have a few years ago.

The final risk of conservative investing is the instinct to do less. However, portfolio allocations always add up to 100%, so doing less of one thing means doing more of another. A thoughtfully constructed conservative portfolio spreads risk across multiple imperfect hedges: intermediate Treasuries, TIPS, gold, minimum volatility equities, international diversification, and real assets. The resulting portfolio will not perfectly hedge any single scenario, but is designed to resilient across many scenarios.

Equities and the AI Transition

From build-out to implementation

We have been writing for a year that AI is transitioning from a build-out phase, characterized by massive capital expenditure and concentrated returns among a handful of enablers, to an implementation phase in which productivity gains diffuse across the broader economy. This has resulted in dramatic declines in the value of numerous software companies deemed to be at risk from AI. What is less obvious is this loss is offset by the gains to companies switching to superior solutions, built either internally or from new startups. This net economic gain is positive, and over time, so will be the return to a broadly diversified global equity investor.

China as an AI hedge

Chinese technology firms can benefit a global portfolio as a partially independent exposure to AI growth. China has the scale, talent, capital, and incentive to compete in AI, and its firms operate in a policy environment largely uncorrelated with U.S. regulation and trade relationships. In the short term, China and US Tech will often be correlated. We saw this in the first quarter, when Chinese technology stocks fell along with U.S. technology due to broader AI repricing. However, the decline for China was muted and even small daily deviations can result in significant long-term diversification. And the longer-term correlation has been lower. Fundamentally, diversification will happen if the underlying investments are different, and it’s clear that the long-term prospects for US and Chinese tech companies have the potential to deviate significantly. Holding both provides exposure to the similar long term growth potential story without the risk of having to pick the winner.

Alternatives: Private Markets

Setting expectations for private markets

Since the early efforts to expand access to private markets, it was clear that investor expectations would need to be reset. The high historical returns to private investments were due to a scarcity of capital, and a large increase in capital would compress returns, increase volatility, and produce pockets of disappointment among individual funds. This is evident today in the private credit market.

Private assets may have a viable future, but to do so they need to transform from the niche funds of the past and converge toward public market return profiles that accompany any asset class as it scales. Private credit funds that are well-diversified, manage credit risk rigorously, and charge reasonable fees will continue to serve a useful role. The funds that were promising public-equity-like returns for a private-debt level of risk were effectively structured to disappoint.

The Two Sides of the Private Markets

On one side, major funds are experiencing redemptions and asset managers who rode the wave up are facing difficult client conversations. On the other, platforms, broker-dealers, custodians, and the largest asset managers continue to push hard to expand retail access to private markets. Both things can be true, but it raises the question of whether the long-run direction is really mass democratization or cautious retrenchment.

Our view is that mass access is eventually coming but that the industry needs to solve a problem it has not yet solved. Private equity today looks structurally like active management in the 1960s and 70s: high fees, high manager dispersion, concentrated portfolios, and an implicit promise that the manager is smarter than the market. Active public equity evolved away from that model over decades, arriving at broad, transparent, low-cost, well-diversified funds that represent the asset class rather than trying to beat it. Private equity has not made that transition yet. A genuine “total private market” fund—broadly diversified, transparent, charging a reasonable fee—would be a real innovation, but no one is offering one at scale today, partly because managers prefer the richer economics of the old model and partly because platforms prefer products with richer sponsorship payouts.

Private credit is a slightly easier case because diversification is already well understood in broader fixed income. Whether the market can distinguish well-managed funds from poorly-managed ones, though, remains an open question. If it cannot, the asset class will suffer through episodes like the current one until the weaker vehicles are washed out.

Gold and bitcoin share the conceptual similarities of scarcity and independence from financial institutions, but have behaved very differently under stress. Gold’s volatility has increased with its success, but tends to hold value in a crisis; bitcoin tends to lose it.

Look Ahead

While anything is possible with a prolonged war, a political Fed, global isolationist nationalism, and an AI future with a diminished role for humans in the economy, the overwhelmingly likely scenario is that the invisible hand of capitalism will find a balance of these often-competing economic forces. As we have seen with tariffs, conflict and technology shocks of the past, the innovation and adaptability of markets ultimately prevails.

Conclusion

The first quarter demonstrated how rapidly market sentiment can pivot, shifting focus from tariff risks to energy shocks in a matter of days. In times of crisis, short-term asset correlations often converge toward one, tempting investors to react tactically.

However, the underlying structural reality of the global economy persists regardless of the daily news cycle. This is not an environment that rewards simple rules or concentrated bets. The era of easy returns is likely over. By prioritizing true global diversification and optimizing portfolios to weather a range of market environments, we ensure that our strategies are positioned for whatever the future brings