Markets reacted to the unveiling of the Trump tariff plan last Wednesday with a broad selloff and continued volatility. The strong reaction was due to several factors. The tariffs were broader than expected – they covered nearly all goods across nearly all countries. They were higher than expected – 20% or more for most major trade partners and 54% for China. They created more uncertainty than expected – their extreme levels left markets uncertain on how long they will last. Finally, they were more economically impactful than expected – the uncertainty and potential severity pose risk of both inflation and economic slowdown.

The economic disruption from tariffs does not have a clear solution. Markets were expecting reciprocal tariffs, which could in theory be negotiated down. Instead, countries are faced with tariffs based on their trade balance with the U.S., which cannot easily be solved. Individual companies acting in their own best interest may have incentives which could worsen the imbalance. For example, foreign manufacturers may source components outside the U.S. where supply chains are less impacted by tariffs, exacerbating the imbalance.

Takeaway:

- Markets interpret available information and form expectations by weighing future scenarios. By design, today’s prices are between the best case (quick resolution) and a worst case (prolonged and expanded trade war). Therefore, markets could quickly recover if policies change.

Some asset classes are more tariff-resilient than others. Selecting the right assets (in the right proportion) for a portfolio is challenging when recession, inflation, and global stability are all in question. Fortunately, intrinsically low-risk assets such as short-term Treasury bills and notes still have relatively high yield, making them a valuable part of the portfolio. Other defensive assets like gold and intermediate and long-term Treasurys, while more volatile, also contribute to managing risk in a portfolio. However, Treasury bonds are at risk due to inflation over time, making TIPS a more suitable defensive asset.

All equities have risk, but markets should also provide a return premium for taking that risk. Two equity ETFs that may be better positioned for current volatility are emerging markets and minimum volatility international equities. Emerging markets are structurally diversified with countries in highly different situations such as China, India, Brazil and Saudi Arabia. Whereas Min Vol ETFs are actively optimized across countries, sectors and companies which avoids some of the most pronounced risks.

Takeaways:

- Nearly all assets are riskier than normal, but some are relatively less so.

- Fixed income ETFs such as Treasurys, particularly Treasury Floating Rate Notes and TIPS can reduce portfolio risk.

- All equities are experiencing substantially higher than usual volatility, but ETFs such as Emerging Markets and Min Vol International may be less exposed to today’s uncertainty.

Managing risk: how to invest now. The first defense against market surprises is a portfolio that is already well diversified geographically, and among many asset classes. However, a more sophisticated investing approach has additional benefits during a crisis. Equity risk is very high, but fixed income, while more volatile than usual, is still relatively safe compared to other assets. High volatility does not mean that we can predict the direction of markets. Markets are reasonably good at including available information into prices, and therefore return expectations for risky assets should always be priced so they have a higher expected future return than safer assets – this is reinforced by economic theory and even history.

Refer to our previous blog: Pulling Out of Volatile Markets Can Lead to Lost Gains - New Frontier Advisors - Commentaries - Advisor Perspectives

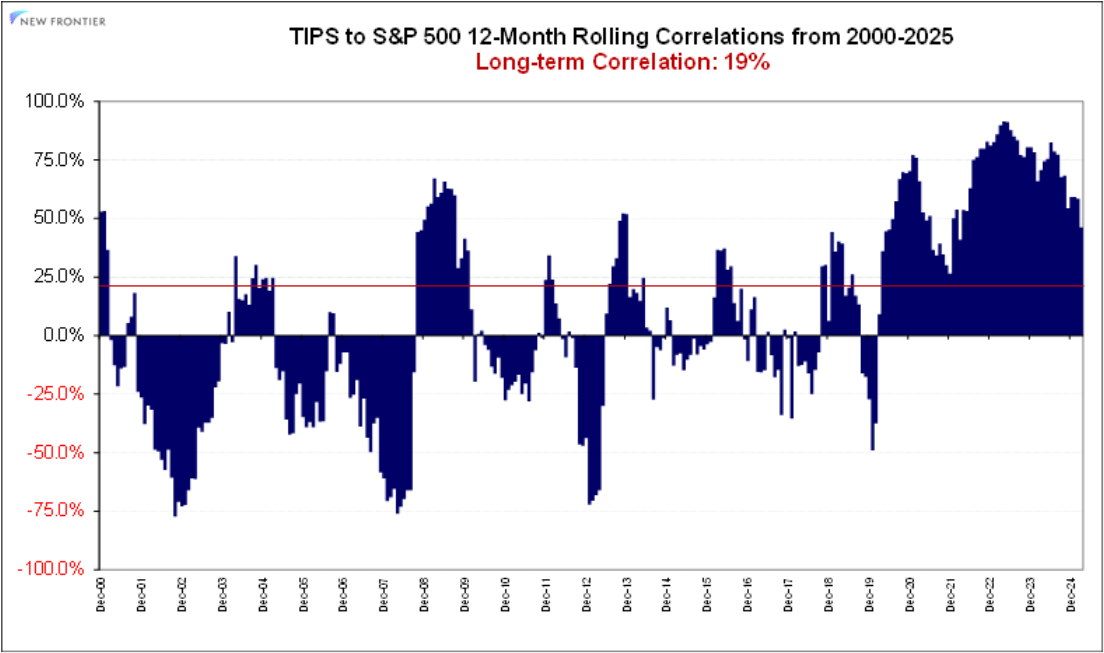

So, while it may be unproductive to forecast returns, it is irresponsible to ignore changes in risk and correlation. For example, TIPS correlation changes over time and deviates from its long-term correlation.

Source: ETF monthly return data 1/31/2000 – 3/31/2025 sourced from Bloomberg; New Frontier

Takeaways:

- Staying invested through volatility has historically been the best answer.

- Investors may wish to have somewhat less risk now than normal, but the market has already rebalanced through lower prices of the riskiest assets.

- It is generally not a good idea to take additional risk in search of high returns during a period of high volatility, as outcomes vary widely.

- A sophisticated approach where the portfolio adjusts to new risk relationships can mitigate risk in volatile times.

- New Frontier portfolios are always optimized for an uncertain future with ETF holdings diversified across regions and asset classes.

Private assets are not the answer for volatile times. Private assets have become more available to investors through retail focused funds and even ETFs. While private assets may seem less volatile due to their longer investment horizon, they are no less, and often more, risky than their public counterparts.

The right allocation to private assets depends on the goal of the investor, but it’s helpful to consider the average investor first, and then decide whether it’s appropriate to have more or less exposure than average. Summing up all publicly traded stocks and bonds, the global market portfolio often has roughly a 60/40 split. Currently, private equity and credit are in the order of $10 trillion and $2 trillion respectively. Compared to well over $100 trillion for each of the public counterparts, this translates into roughly a 5% weight for private assets in the average investor’s portfolio.

Takeaways:

- Depending on what you count, private assets are only ~5% of the total market. So a 20% allocation is clearly an over allocation. Sometimes it’s ok to over allocate, but you should understand the reason for the over allocation.

- There’s no rush to get into private assets during a volatility crisis.